In finance, a put or put option is a financial market derivative instrument which gives the holder the right to sell an asset, at a specified price, by a specified date to the writer of the put. The purchase of a put option is interpreted as a negative sentiment about the future value of the underlying stock. The term "put" comes from the fact that the owner has the right to "put up for sale" the stock or index.

An exchange-traded fund (ETF) is a type of investment fund and exchange-traded product, i.e. they are traded on stock exchanges. ETFs are similar in many ways to mutual funds, except that ETFs are bought and sold throughout the day on stock exchanges while mutual funds are bought and sold based on their price at day's end. An ETF holds assets such as stocks, bonds, currencies, and/or commodities such as gold bars, and generally operates with an arbitrage mechanism designed to keep it trading close to its net asset value, although deviations can occasionally occur. Most ETFs are index funds: that is, they hold the same securities in the same proportions as a certain stock market index or bond market index. The most popular ETFs in the U.S. replicate the S&P 500 Index, the total market index, the NASDAQ-100 index, the price of gold, the "growth" stocks in the Russell 1000 Index, or the index of the largest technology companies. With the exception of non-transparent actively managed ETFs, in most cases, the list of stocks that each ETF owns, as well as their weightings, is posted daily on the website of the issuer. The largest ETFs have annual fees of 0.03% of the amount invested, or even lower, although specialty ETFs can have annual fees well in excess of 1% of the amount invested. These fees are paid to the ETF issuer out of dividends received from the underlying holdings or from selling assets.

In finance, the beta is a measure of how an individual asset moves when the overall stock market increases or decreases. Thus, beta is a useful measure of the contribution of an individual asset to the risk of the market portfolio when it is added in small quantity. Thus, beta is referred to as an asset's non-diversifiable risk, its systematic risk, market risk, or hedge ratio. Beta is not a measure of idiosyncratic risk.

In finance, the Sharpe ratio measures the performance of an investment compared to a risk-free asset, after adjusting for its risk. It is defined as the difference between the returns of the investment and the risk-free return, divided by the standard deviation of the investment. It represents the additional amount of return that an investor receives per unit of increase in risk.

The Chicago Board Options Exchange (CBOE), located at 400 South LaSalle Street in Chicago, is the largest U.S. options exchange with annual trading volume that hovered around 1.27 billion contracts at the end of 2014. CBOE offers options on over 2,200 companies, 22 stock indices, and 140 exchange-traded funds (ETFs).

MSCI Inc., is an American finance company headquartered in New York City and serving as a global provider of equity, fixed income, hedge fund stock market indexes, multi-asset portfolio analysis tools and ESG products. It publishes the MSCI BRIC, MSCI World and MSCI EAFE Indexes.

The MSCI World is a market cap weighted stock market index of 1,583 companies throughout the world. It is maintained by MSCI, formerly Morgan Stanley Capital International, and is used as a common benchmark for 'world' or 'global' stock funds intended to represent a broad cross-section of global markets.

An option symbol is a code by which options are identified on an options exchange or a futures exchange.

The information ratio, also known as appraisal ratio, measures and compares the active return of an investment compared to a benchmark index relative to the volatility of the active return. It is defined as the active return divided by the tracking error. It represents the additional amount of return that an investor receives per unit of increase in risk. The information ratio is simply the ratio of the active return of the portfolio divided by the tracking error of its return, with both components measured relative to the performance of the agreed-on benchmark.

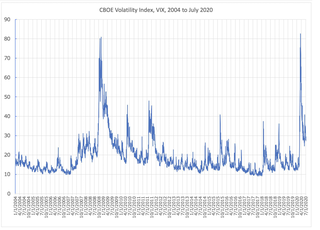

VIX is the ticker symbol and the popular name for the Chicago Board Options Exchange's CBOE Volatility Index, a popular measure of the stock market's expectation of volatility based on S&P 500 index options. It is calculated and disseminated on a real-time basis by the CBOE, and is often referred to as the fear index or fear gauge.

iShares is a collection of exchange-traded funds (ETFs) managed by BlackRock, which acquired the brand and business from Barclays in 2009. The first iShares ETFs were known as World Equity Benchmark Shares (WEBS) but have since been rebranded.

The Bloomberg Barclays US Aggregate Bond Index, or the Agg, is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. Investors frequently use the index as a stand-in for measuring the performance of the US bond market.

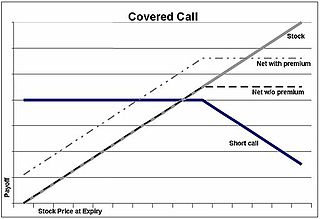

A covered call is a financial market transaction in which the seller of call options owns the corresponding amount of the underlying instrument, such as shares of a stock or other securities. If a trader buys the underlying instrument at the same time the trader sells the call, the strategy is often called a "buy-write" strategy. In equilibrium, the strategy has the same payoffs as writing a put option.

The CBOE S&P 500 BuyWrite Index is a benchmark index designed to show the hypothetical performance of a portfolio that engages in a buy-write strategy using S&P 500 index call options.

In finance, an option is a contract which conveys its owner, the holder, the right, but not the obligation, to buy or sell an underlying asset or instrument at a specified strike price prior to or on a specified date, depending on the form of the option. Options are typically acquired by purchase, as a form of compensation, or as part of a complex financial transaction. Thus, they are also a form of asset and have a valuation that may depend on a complex relationship between underlying asset value, time until expiration, market volatility, and other factors. Options may be traded between private parties in over-the-counter (OTC) transactions, or they may be exchange-traded in live, orderly markets in the form of standardized contracts.

The CBOE S&P DJIA BuyWrite Index is a benchmark index designed to show the hypothetical performance of a portfolio that engages in a buy-write strategy on the Dow Jones Industrial Average (DJIA).

Post-modern portfolio theory is an extension of the traditional modern portfolio theory. Both theories propose how rational investors should use diversification to optimize their portfolios, and how a risky asset should be priced.

The term buy-write is used to describe an investment strategy in which the investor buys stocks and writes call options against the stock position. The writing of the call option provides extra income for an investor who is willing to forgo some upside potential.