In the United States, redlining is the systematic denial of various services to residents of specific, often racially associated, neighborhoods or communities, either explicitly or through the selective raising of prices. While the best known examples of redlining have involved denial of financial services such as banking or insurance, other services such as health care or even supermarkets have been denied to residents. In the case of retail businesses like supermarkets, purposely locating stores impractically far away from targeted residents results in a redlining effect.

The United States Department of Housing and Urban Development (HUD) is a Cabinet department in the executive branch of the U.S. federal government. Although its beginnings were in the House and Home Financing Agency, it was founded as a Cabinet department in 1965, as part of the "Great Society" program of President Lyndon B. Johnson, to develop and execute policies on housing and metropolises.

This aims to be a complete list of the articles on real estate.

A housing cooperative, or housing co-op, is a legal entity, usually a cooperative or a corporation, which owns real estate, consisting of one or more residential buildings; it is one type of housing tenure. Housing cooperatives are a distinctive form of home ownership that have many characteristics that differ from other residential arrangements such as single family home ownership, condominiums and renting.

A reverse mortgage is a mortgage loan, usually secured by a residential property, that enables the borrower to access the unencumbered value of the property. The loans are typically promoted to older homeowners and typically do not require monthly mortgage payments. Borrowers are still responsible for property taxes and homeowner's insurance. Reverse mortgages allow elders to access the home equity they have built up in their homes now, and defer payment of the loan until they die, sell, or move out of the home. Because there are no required mortgage payments on a reverse mortgage, the interest is added to the loan balance each month. The rising loan balance can eventually grow to exceed the value of the home, particularly in times of declining home values or if the borrower continues to live in the home for many years. However, the borrower is generally not required to repay any additional loan balance in excess of the value of the home.

An FHA insured loan is a US Federal Housing Administration mortgage insurance backed mortgage loan that is provided by an FHA-approved lender. FHA mortgage insurance protects lenders against losses. They have historically allowed lower-income Americans to borrow money to purchase a home that they would not otherwise be able to afford. Because this type of loan is more geared towards new house owners than real estate investors, FHA loans are different from conventional loans in the sense that the house must be owner-occupant for at least a year. Since loans with lower down-payments usually involve more risk to the lender, the home-buyer must pay a two-part mortgage insurance that involves a one-time bulk payment and a monthly payment to compensate for the increased risk. Frequently, individuals "refinance" or replace their FHA loan to remove their monthly mortgage insurance premium. Removing mortgage insurance premium by paying down the loan has become more difficult with FHA loans as of 2013.

The Community Reinvestment Act is a United States federal law designed to encourage commercial banks and savings associations to help meet the needs of borrowers in all segments of their communities, including low- and moderate-income neighborhoods. Congress passed the Act in 1977 to reduce discriminatory credit practices against low-income neighborhoods, a practice known as redlining.

Canada Mortgage and Housing Corporation (CMHC) is a Crown Corporation of the Government of Canada. It was originally established after World War II, to help returning war veterans find housing. It has since expanded its mandate to assist housing for all Canadians. The organization's primary goals are to provide mortgage liquidity, assist in affordable housing development, and provide unbiased research and advice to the Canadian government, and housing industry.

The Rural Housing Service (RHS) is an agency of the United States Department of Agriculture (USDA). Located within the Department's Rural Development mission area. RHS operates a broad range of programs to provide moderate- low- and very-low-income Americans in rural communities with:

A VA loan is a mortgage loan in the United States guaranteed by the United States Department of Veterans Affairs (VA). The program is for American veterans, military members currently serving in the U.S. military, reservists and select surviving spouses and can be used to purchase single-family homes, condominiums, multi-unit properties, manufactured homes and new construction. The VA does not originate loans, but sets the rules for who may qualify, issues minimum guidelines and requirements under which mortgages may be offered and financially guarantees loans that qualify under the program.

Subsidized housing is government sponsored economic assistance aimed towards alleviating housing costs and expenses for impoverished people with low to moderate incomes. In the United States, subsidized housing is often called "affordable housing." Forms of subsidies include direct housing subsidies, non-profit housing, public housing, rent supplements/vouchers, and some forms of co-operative and private sector housing. According to some sources, increasing access to housing may contribute to lower poverty rates.

The Housing and Community Development Act of 1974,, is a United States federal law that, among other provisions, amended the Housing Act of 1937 to create Section 8 housing, authorizes "Entitlement Communities Grants" to be awarded by the United States Department of Housing and Urban Development, and created the National Institute of Building Sciences. Under Section 810 of the Act the first federal Urban Homesteading program was created.

A mortgage loan or simply mortgage is a loan used either by purchasers of real property to raise funds to buy real estate, or alternatively by existing property owners to raise funds for any purpose while putting a lien on the property being mortgaged. The loan is "secured" on the borrower's property through a process known as mortgage origination. This means that a legal mechanism is put into place which allows the lender to take possession and sell the secured property to pay off the loan in the event the borrower defaults on the loan or otherwise fails to abide by its terms. The word mortgage is derived from a Law French term used in Britain in the Middle Ages meaning "death pledge" and refers to the pledge ending (dying) when either the obligation is fulfilled or the property is taken through foreclosure. A mortgage can also be described as "a borrower giving consideration in the form of a collateral for a benefit (loan)".

Housing segregation in the United States is the practice of denying African Americans and other minority groups equal access to housing through the process of misinformation, denial of realty and financing services, and racial steering. Housing policy in the United States has influenced housing segregation trends throughout history. Key legislation include the National Housing Act of 1934, the G.I. Bill, and the Fair Housing Act. Factors such as socioeconomic status, spatial assimilation, and immigration contribute to perpetuating housing segregation. The effects of housing segregation include relocation, unequal living standards, and poverty. However, there have been initiatives to combat housing segregation, such as the Section 8 housing program.

The United States Housing and Economic Recovery Act of 2008 was designed primarily to address the subprime mortgage crisis. It authorized the Federal Housing Administration to guarantee up to $300 billion in new 30-year fixed rate mortgages for subprime borrowers if lenders wrote down principal loan balances to 90 percent of current appraisal value. It was intended to restore confidence in Fannie Mae and Freddie Mac by strengthening regulations and injecting capital into the two large U.S. suppliers of mortgage funding. States are authorized to refinance subprime loans using mortgage revenue bonds. Enactment of the Act led to the government conservatorship of Fannie Mae and Freddie Mac.

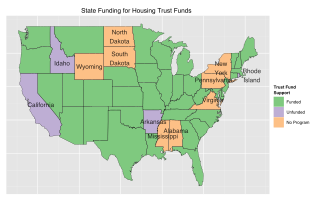

Housing trust funds are established sources of funding for affordable housing construction and other related purposes created by governments in the United States (U.S.). Housing Trust Funds (HTF) began as a way of funding affordable housing in the late 1970s. Since then, elected government officials from all levels of government in the U.S. have established housing trust funds to support the construction, acquisition, and preservation of affordable housing and related services to meet the housing needs of low-income households. Ideally, HTFs are funded through dedicated revenues like real estate transfer taxes or document recording fees to ensure a steady stream of funding rather than being dependent on regular budget processes. As of 2016, 400 state, local and county trust funds existed across the U.S.

The Housing and Urban Development Act of 1968, Pub.L. 90–448, 82 Stat. 476, enacted August 1, 1968, was passed during the Lyndon B. Johnson Administration. The act came on the heels of major riots across cities throughout the U.S. in 1967, the assassination of Civil Rights Leader Martin Luther King Jr. in April 1968, and the publication of the report of the Kerner Commission, which recommended major expansions in public funding and support of urban areas. President Lyndon B. Johnson referred to the legislation as one of the most significant laws ever passed in the U.S., due to its scale and ambition. The act's declared intention was constructing or rehabilitating 26 million housing units, 6 million of these for low- and moderate-income families, over the next 10 years.

A USDA Home Loan from the USDA loan program, also known as the USDA Rural Development Guaranteed Housing Loan Program, is a mortgage loan offered to rural property owners by the United States Department of Agriculture.

Live Well Financial, Inc. ("LWF") was a privately owned mortgage originator, servicer and investor, licensed in the United States to operate in 46 states. The company offered government-insured Home Equity Conversion Mortgage loans, FHA single family mortgage loans, and Fannie Mae conforming loans. LWF is headquartered in Richmond, Virginia and has 3 retail origination branches, 2 in Richmond, Virginia and 1 in San Diego, California, with origination capabilities throughout the United States. The company and its principals are now the focus of criminal and civil charges alleging a large-scale financial fraud.

Affordable housing is housing which is deemed affordable to those with a median household income as rated by the national government or a local government by a recognized housing affordability index. The challenges of promoting affordable housing varies by location.