Related Research Articles

In economics, a recession is a business cycle contraction that occurs when there is a general decline in economic activity. Recessions generally occur when there is a widespread drop in spending. This may be triggered by various events, such as a financial crisis, an external trade shock, an adverse supply shock, the bursting of an economic bubble, or a large-scale anthropogenic or natural disaster.

An interest rate is the amount of interest due per period, as a proportion of the amount lent, deposited, or borrowed. The total interest on an amount lent or borrowed depends on the principal sum, the interest rate, the compounding frequency, and the length of time over which it is lent, deposited, or borrowed.

The 1997 Asian financial crisis was a period of financial crisis that gripped much of East and Southeast Asia during the late 1990s. The crisis began in Thailand in July 1997 before spreading to several other countries with a ripple effect, raising fears of a worldwide economic meltdown due to financial contagion. However, the recovery in 1998–1999 was rapid, and worries of a meltdown quickly subsided.

Within the budgetary process, deficit spending is the amount by which spending exceeds revenue over a particular period of time, also called simply deficit, or budget deficit; the opposite of budget surplus. The term may be applied to the budget of a government, private company, or individual. Government deficit spending was first identified as a necessary economic tool by John Maynard Keynes in the wake of the Great Depression. It is a central point of controversy in economics, as discussed below.

The government budget balance, also alternatively referred to as general government balance, public budget balance, or public fiscal balance, is the overall difference between government revenues and spending. A positive balance is called a government budget surplus, and a negative balance is a government budget deficit. A government budget is a financial statement presenting the government's proposed revenues and spending for a financial year. A budget is prepared for each level of government and takes into account public social security obligations.

The national debt of the United States is the total national debt owed by the federal government of the United States to Treasury security holders. The national debt at any point in time is the face value of the then-outstanding Treasury securities that have been issued by the Treasury and other federal agencies. The terms "national deficit" and "national surplus" usually refer to the federal government budget balance from year to year, not the cumulative amount of debt. In a deficit year the national debt increases as the government needs to borrow funds to finance the deficit, while in a surplus year the debt decreases as more money is received than spent, enabling the government to reduce the debt by buying back some Treasury securities. In general, government debt increases as a result of government spending and decreases from tax or other receipts, both of which fluctuate during the course of a fiscal year. There are two components of gross national debt:

In economics, hot money is the flow of funds from one country to another in order to earn a short-term profit on interest rate differences and/or anticipated exchange rate shifts. These speculative capital flows are called "hot money" because they can move very quickly in and out of markets, potentially leading to market instability.

Austerity is a set of political-economic policies that aim to reduce government budget deficits through spending cuts, tax increases, or a combination of both. There are three primary types of austerity measures: higher taxes to fund spending, raising taxes while cutting spending, and lower taxes and lower government spending. Austerity measures are often used by governments that find it difficult to borrow or meet their existing obligations to pay back loans. The measures are meant to reduce the budget deficit by bringing government revenues closer to expenditures. Proponents of these measures state that this reduces the amount of borrowing required and may also demonstrate a government's fiscal discipline to creditors and credit rating agencies and make borrowing easier and cheaper as a result.

The Mexican peso crisis was a currency crisis sparked by the Mexican government's sudden devaluation of the peso against the U.S. dollar in December 1994, which became one of the first international financial crises ignited by capital flight.

Foreign exchange reserves are cash and other reserve assets such as gold held by a central bank or other monetary authority that are primarily available to balance payments of the country, influence the foreign exchange rate of its currency, and to maintain confidence in financial markets. Reserves are held in one or more reserve currencies, nowadays mostly the United States dollar and to a lesser extent the euro.

Household debt is the combined debt of all people in a household, including consumer debt and mortgage loans. A significant rise in the level of this debt coincides historically with many severe economic crises and was a cause of the U.S. and subsequent European economic crises of 2007–2012. Several economists have argued that lowering this debt is essential to economic recovery in the U.S. and selected Eurozone countries.

Structural adjustment programs (SAPs) consist of loans provided by the International Monetary Fund (IMF) and the World Bank (WB) to countries that experience economic crises. Their purpose is to adjust the country's economic structure, improve international competitiveness, and restore its balance of payments.

The Convertibility plan was a plan by the Argentine Currency Board that pegged the Argentine peso to the U.S. dollar between 1991 and 2002 in an attempt to eliminate hyperinflation and stimulate economic growth. While it initially met with considerable success, the board's actions ultimately failed. In contrast to what most people think, this peg actually did not exist, except only in the first years of the plan. From then on, the government never needed to use the foreign exchange reserves of the country in the maintenance of the peg, except when the recession and the massive bank withdrawals started in 2000.

In economics, the debt-to-GDP ratio is the ratio between a country's government debt and its gross domestic product (GDP). A low debt-to-GDP ratio indicates that an economy produces goods and services sufficient to pay back debts without incurring further debt. Geopolitical and economic considerations – including interest rates, war, recessions, and other variables – influence the borrowing practices of a nation and the choice to incur further debt.

The real interest rate is the rate of interest an investor, saver or lender receives after allowing for inflation. It can be described more formally by the Fisher equation, which states that the real interest rate is approximately the nominal interest rate minus the inflation rate.

Capital controls are residency-based measures such as transaction taxes, other limits, or outright prohibitions that a nation's government can use to regulate flows from capital markets into and out of the country's capital account. These measures may be economy-wide, sector-specific, or industry specific. They may apply to all flows, or may differentiate by type or duration of the flow.

At the micro-economic level, deleveraging refers to the reduction of the leverage ratio, or the percentage of debt in the balance sheet of a single economic entity, such as a household or a firm. It is the opposite of leveraging, which is the practice of borrowing money to acquire assets and multiply gains and losses.

The financial position of the United States includes assets of at least $269.6 trillion and debts of $145.8 trillion to produce a net worth of at least $123.8 trillion as of Q1 2014.

Carmen M. Reinhart is a Cuban-American economist and the Minos A. Zombanakis Professor of the International Financial System at Harvard Kennedy School. Previously, she was the Dennis Weatherstone Senior Fellow at the Peterson Institute for International Economics and Professor of Economics and Director of the Center for International Economics at the University of Maryland. She is a research associate at the National Bureau of Economic Research, a Research Fellow at the Centre for Economic Policy Research, Founding Contributor of VoxEU, and a member of Council on Foreign Relations. She is also a member of American Economic Association, Latin American and Caribbean Economic Association, and the Association for the Study of the Cuban Economy. She became the subject of general news coverage when mathematical errors were found in a research paper she co-authored.

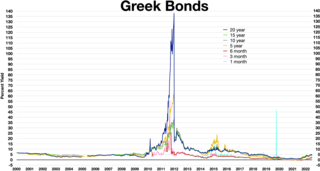

Greece faced a sovereign debt crisis in the aftermath of the financial crisis of 2007–2008. Widely known in the country as The Crisis, it reached the populace as a series of sudden reforms and austerity measures that led to impoverishment and loss of income and property, as well as a small-scale humanitarian crisis. In all, the Greek economy suffered the longest recession of any advanced mixed economy to date. As a result, the Greek political system has been upended, social exclusion increased, and hundreds of thousands of well-educated Greeks have left the country.

References

- 1 2 3 4 "China Savers Prioritized Over Banks by PBOC". Bloomberg. November 25, 2014.

- 1 2 3 4 Carmen M. Reinhart, Jacob F. Kirkegaard, and M. Belen Sbrancia, "Financial Repression Redux", IMF Finance and Development, June 2011, p. 22-26

- ↑ Shaw, Edward S. Financial Deepening in Economic Development. New York: Oxford University Press, 1973

- ↑ McKinnon, Ronald I. Money and Capital in Economic Development. Washington, D.C.: Brookings Institution, 1973

- 1 2 3 Carmen M. Reinhart and M. Belen Sbrancia, "The Liquidation of Government Debt", IMF, 2011, p. 19

- ↑ Reinhart, Carmen M. and Rogoff, Kenneth S., This Time is Different: Eight Centuries of Financial Folly. Princeton and Oxford: Princeton University Press, 2008, p. 143

- ↑ Bill Gross, "The Caine Mutiny Part 2", PIMCO

- ↑ Giovannini, Alberto and de Melo, Martha, "Government Revenue from Financial Repression", The American Economic Review , Vol. 83, No. 4 Sep. 1993 (pp. 953-963)

- ↑ "The great repression". The Economist. 16 June 2011.

- 1 2 "Financial Repression 101". Allianz Global Investors. Retrieved 2 December 2014.

- ↑ cf. Paul Krugman's point of view: Secular Stagnation, Coalmines, Bubbles, and Larry Summers, The New York Times, November 16th, 2013, retrieved November 28th, 2013: „[…] a situation in which the 'natural' rate of interest – the rate at which desired savings and desired investment would be equal at full employment – is negative. […] when looking forward you have to regard the liquidity trap not as an exceptional state of affairs but as the new normal.“ cf. also: Larry Summers at IMF Economic Forum, Nov. 8, YouTube, published on November 8th, 2013, retrieved on November 28th, 2013: Larry Summers said there: „imagine a situation where natural and equilibrium interest rate have fallen significantly below zero.“

- ↑ Gillian Tett, "Policymakers learn a new and alarming catchphrase", Financial Times, May 9, 2011

- ↑ Amerman, Daniel (September 12, 2011). "The 2nd Edge of Modern Financial Repression: Manipulating Inflation Indexes to Steal from Retirees & Public Workers". Financial Sense.