World's first major period of globalization of trade and finance

A German railway in 1895.A telegraph used to emit in morse code.The ocean linerSS Kaiser Wilhelm der Grosse, a steamboat. As the main means of transo oceanic travel for more than a century, ocean liners were essential to the transport needs of national governments, commercial enterprises and the general public.

"First globalization" is a phrase used by economists to describe the world's first major period of globalization of trade and finance, which took place between 1870 and 1914. The "second globalization" began in 1944 and ended in 1971. This led to the third era of globalization, which began in 1989 and continues today.[1]

The period from 1870 to 1914 represents the peak of 19th-century globalization. First globalization is known for increasing transfers of commodities, people, capital and labour between and within continents. However, it is not only about the movement of goods or factors of production. First globalization also includes technological transfers and the rise of international cultural and scientific cooperation. The 1876 World Fair in Philadelphia was the first not to take place in Europe. The modern Olympics began in 1896. The first Nobel prizes were awarded in 1901.[2][3][4]

International trade grew for many reasons. Constant technological improvement and increased usage associated with the decline in international freight rates. The development of railways lowered the transport costs, which resulted in a massive migration within Europe and from the Old World to the New World. Exchange-trade stability and reduction of uncertainty in trade made possible by the gold standard. Peace between main powers and reduction of trade barriers promoted trade.[2][3][4]

1870-1914 is also known as the laissez-faire period, thus mostly liberal international policies are in place. However, the trade policies of the time lacked reciprocity.[3]

This period saw financial crises comparable to those of the late twentieth and early twenty-first centuries and the end of the First globalisation is associated with the collapse of international trade when World War I. started.[3]

Globalization revolves around technological and social advances, which further leads to advances in trade and cultural relativism throughout the world. Some economists claim that globalization was first started by the discovery of the Americas by Christopher Columbus. This assumption is considered false due to the mass discovery of gold and silver in mines. This discovery led to the decrease in value of silver and gold in Europe, causing inflation in the Spanish and Portuguese empires.[5] However, the discovery of the Americas and the natives gave European traders a new source of labor between the continents, which also increased trade. This stage has not been officially deemed the "first era of globalization" because the world trade numbers were not increasing exponentially. World trade increased by 1% per year from 1500 to 1800, which further led to the first era of globalization.[6]

Entering the 18th century, due to new technological breakthroughs world trade started to increase rapidly. The first technological advancement that contributed to this was the steam engine, introduced in the 17th century. This led to major progress in international trade among the economic powers of the world.[7]

The invention of the steamship had a great impact on the first wave of globalization. Before its invention, trade routes were reliant on wind patterns, but steamships reduced shipping time and shipping cost. By 1850, nearly 129 countries used steamships for trade, and approximately 5,000 imports and exports were made to 5,000 cities, thus making a great impact on the world's global economy.[8]

Trade

Integration during the First globalization period can be demonstrated in many ways. The volume of international flows, the ratio of commodity trade to GDP and the cost of moving goods or factors of production across borders are a few of the measures, which help us show the increasing trade trend between 1870 and 1914. The third mentioned measure shows up in the international price gaps and for example, the price gap of wheat between Liverpool and Chicago fell from 57,6% to 15,6%, and the price gap of bacon between London and Cincinnati fell from 92,5% to 17,9%.[2]

Many factors contributed to the growth of international trade. Falling transportation cost, reduction of trade barriers and move to free trade in several countries are just a few of those factors. Europe was a net exporter of manufacturers and a net importer of primary products. New World exchanged food and raw materials for European manufactured goods. This ended up being beneficial for European workers because, in the era where a large portion of income was still spent on food, cheaper transport meant cheaper food and thus higher real wages. However, it was not so beneficial for farmers. Only in countries that retained agricultural free trade, like the United Kingdom, were less vulnerable to the price and rent reductions that globalization implied. Trade between industrialized economies was the prevalent form of trade before 1914.[2][3][4]

However, tariff levels were not unchanging throughout the period. During the late 1880s and early 1890s, there was a pronounced protectionist backlash against globalisation, in which nearly all industrial and settler economies participated.[9] This overseas protectionism was injurious to the export sector of the United Kingdom, with one study estimating that British exports would have been 57% higher if the foreign countries had embraced free trade rather than protection.[10]

Capital

International capital market integration was impressive during this period. By 1914, foreign assets accounted for nearly 20% of the worlds GDP. A figure, that was not measured again until the 1970s. Europe was the main moving power. In 1914, over 87% of total foreign investment belonged to European countries. While economic institutions and policies helped with the expend of international capital integration, the absence of military conflict between main lending countries and reduction in exchange-rate risk and transaction due to the gold standard kicked off the trend.[2][3]

Investment went in economies with exploitable natural resources rather than economies with cheap labour. The target was not to internationalize production but to facilitate access to raw materials, which Europe was not able to produce in great quantities. Therefore, international investment was highly concentrated. Investment mainly went into the construction of railways, land improvement, housing and other social projects that made it more pleasant for workers and beneficial for European consumers.[2][3]

The increase in capital exports raised demand for merchandise exports, and, in this way, factor flows reinforced the growth in trade during the first globalisation.[11]

Migration

Migration was a large part of the First globalization. Migration rates were enormous in European countries like Italy, Greece or Ireland. Migrations were not just transoceanic, but within Europe as well. The fact that American and Australian workers earned higher wages than their European counterparts was the main reason for the mass migrations. Combined with low travel cost and liberal policies, mass migration was inevitable. However, migration had the greatest impact on the European workers living standard during the First Globalization. Lowering the labour supply pushed up real wages. On the other hand, migration hurt their counterparts overseas. Immigration in the United States lowered unskilled wages. This resulted in tightening restrictions on immigration in the main destination countries.[2]

Technology

In Europe and the Atlantic world, technologies had been circulating for a long time and relatively freely in the late 19th century, despite laws forbidding the emigration of skilled workers and machinery exports. The decline in transport and communication costs helped the diffusion of ideas, new goods and machines. The diffusion of technologies was also supported by the creation of international scientific and technical organizations. However, science was seen as one of the weapons in the struggle between European nations. Between France and Germany, each hoped to tighten their links with allied and neutral countries, especially the United States. Later restrictive policies, aimed at import substitution, resulted in firms setting up production in foreign countries and transforming themselves into multinationals.[2]

The period of the First globalization saw the rise and fall of the gold standard. During the trade boom from 1870 to 1914 one country after another joined the gold standard regime, and gradually the system spread. The gold standard allows countries to convert their currencies to gold. This reduces the exchange-rate risk, transaction costs and assures potential investors that returns are reasonably safe.[2][3][4]

The gold standard was the central pillar of the First globalization. Global financial integration collapse in the summer of 1914 saw the fall of the gold standard as well. The final collapse of the gold standard came in the 1930s.[2][4]

After 1914

The beginning of World War I. has associated with a collapse of global financial integration and a decline in trade. The emerging of new borders and a rise in levels of protection shot up to trade barriers that would be still rising after the end of World War I. Meanwhile, tariffs, quotas and other commercial policy barriers were on a rise. Global bodies and international conferences tried to normalize, but governments were unwilling to undo their barriers and after the Imperial Economic Conference in Ottawa in 1932, international cooperation was no longer even an illusion. Interested parties thought that the restoration of the gold standard is a goal worth pursuing. However, after a brief return between 1925 and 1929 came a collapse of the gold standard in the 1930s, which drove trade volumes even lower.[2][4]

↑ Bairoch, Paul; Burke, Susan (1989), Mathias, Peter; Pollard, Sidney (eds.), "European trade policy, 1815–1914", The Cambridge Economic History of Europe from the Decline of the Roman Empire: Volume 8: The Industrial Economies: The Development of Economic and Social Policies, The Cambridge Economic History of Europe, Cambridge: Cambridge University Press, vol.8, pp.1–160, ISBN978-1-139-05450-8, retrieved 2023-05-22

A customs union is generally defined as a type of trade bloc which is composed of a free trade area with a common external tariff.

International trade is the exchange of capital, goods, and services across international borders or territories because there is a need or want of goods or services.

Globalization, or globalisation, is the process of interaction and integration among people, companies, and governments worldwide. The term globalization first appeared in the early 20th century, developed its current meaning sometime in the second half of the 20th century, and came into popular use in the 1990s to describe the unprecedented international connectivity of the post-Cold War world. Its origins can be traced back to 18th and 19th centuries due to advances in transportation and communications technology. This increase in global interactions has caused a growth in international trade and the exchange of ideas, beliefs, and culture. Globalization is primarily an economic process of interaction and integration that is associated with social and cultural aspects. However, disputes and international diplomacy are also large parts of the history of globalization, and of modern globalization.

A tariff is a tax imposed by the government of a country or by a supranational union on imports or exports of goods. Besides being a source of revenue for the government, import duties can also be a form of regulation of foreign trade and policy that taxes foreign products to encourage or safeguard domestic industry. Protective tariffs are among the most widely used instruments of protectionism, along with import quotas and export quotas and other non-tariff barriers to trade.

Free trade is a trade policy that does not restrict imports or exports. In government, free trade is predominantly advocated by political parties that hold economically liberal positions, while economic nationalist and left-wing political parties generally support protectionism, the opposite of free trade.

The economic history of Argentina is one of the most studied, owing to the "Argentine paradox". As a country, it had achieved advanced development in the early 20th century but experienced a reversal relative to other developed economies, which inspired an enormous wealth of literature and diverse analysis on the causes of this relative decline. Since independence from Spain in 1816, the country has defaulted on its debt nine times. Inflation has often risen to the double digits, even as high as 5000%, resulting in several large currency devaluations.

Protectionism, sometimes referred to as trade protectionism, is the economic policy of restricting imports from other countries through methods such as tariffs on imported goods, import quotas, and a variety of other government regulations. Proponents argue that protectionist policies shield the producers, businesses, and workers of the import-competing sector in the country from foreign competitors. Opponents argue that protectionist policies reduce trade, and adversely affect consumers in general as well as the producers and workers in export sectors, both in the country implementing protectionist policies and in the countries against which the protections are implemented.

The global financial system is the worldwide framework of legal agreements, institutions, and both formal and informal economic action that together facilitate international flows of financial capital for purposes of investment and trade financing. Since emerging in the late 19th century during the first modern wave of economic globalization, its evolution is marked by the establishment of central banks, multilateral treaties, and intergovernmental organizations aimed at improving the transparency, regulation, and effectiveness of international markets. In the late 1800s, world migration and communication technology facilitated unprecedented growth in international trade and investment. At the onset of World War I, trade contracted as foreign exchange markets became paralyzed by money market illiquidity. Countries sought to defend against external shocks with protectionist policies and trade virtually halted by 1933, worsening the effects of the global Great Depression until a series of reciprocal trade agreements slowly reduced tariffs worldwide. Efforts to revamp the international monetary system after World War II improved exchange rate stability, fostering record growth in global finance.

An export in international trade is a good produced in one country that is sold into another country or a service provided in one country for a national or resident of another country. The seller of such goods or the service provider is an exporter; the foreign buyers is an importer. Services that figure in international trade include financial, accounting and other professional services, tourism, education as well as intellectual property rights.

In international economics, the balance of payments of a country is the difference between all money flowing into the country in a particular period of time and the outflow of money to the rest of the world. These financial transactions are made by individuals, firms and government bodies to compare receipts and payments arising out of trade of goods and services.

Trade barriers are government-induced restrictions on international trade. According to the theory of comparative advantage, trade barriers are detrimental to the world economy and decrease overall economic efficiency.

The Long Depression was a worldwide price and economic recession, beginning in 1873 and running either through March 1879, or 1896, depending on the metrics used. It was most severe in Europe and the United States, which had been experiencing strong economic growth fueled by the Second Industrial Revolution in the decade following the American Civil War. The episode was labeled the "Great Depression" at the time, and it held that designation until the Great Depression of the 1930s. Though it marked a period of general deflation and a general contraction, it did not have the severe economic retrogression of the Great Depression.

Non-tariff barriers to trade are trade barriers that restrict imports or exports of goods or services through mechanisms other than the simple imposition of tariffs. Such barriers are subject to controversy and debate, as they may comply with international rules on trade yet serve protectionist purposes.

Trade can be a key factor in economic development. The prudent use of trade can boost a country's development and create absolute gains for the trading partners involved. Trade has been touted as an important tool in the path to development by prominent economists. However trade may not be a panacea for development as important questions surrounding how free trade really is and the harm trade can cause domestic infant industries to come into play.

International economics is concerned with the effects upon economic activity from international differences in productive resources and consumer preferences and the international institutions that affect them. It seeks to explain the patterns and consequences of transactions and interactions between the inhabitants of different countries, including trade, investment and transaction.

Economic integration is the unification of economic policies between different states, through the partial or full abolition of tariff and non-tariff restrictions on trade.

Regional Integration is a process in which neighboring countries enter into an agreement in order to upgrade cooperation through common institutions and rules. The objectives of the agreement could range from economic to political to environmental, although it has typically taken the form of a political economy initiative where commercial interests are the focus for achieving broader socio-political and security objectives, as defined by national governments. Regional integration has been organized either via supranational institutional structures or through intergovernmental decision-making, or a combination of both.

Deglobalization or deglobalisation is the process of diminishing interdependence and integration between certain units around the world, typically nation-states. It is widely used to describe the periods of history when economic trade and investment between countries decline. It stands in contrast to globalization, in which units become increasingly integrated over time, and generally spans the time between periods of globalization. While globalization and deglobalization are antitheses, they are not mirror images.

The historical origins of globalization are the subject of ongoing debate. Though many scholars situate the origins of globalization in the modern era, others regard it as a phenomenon with a long history, dating back thousands of years. The period in the history of globalization roughly spanning the years between 1600 and 1800 is in turn known as the proto-globalization.

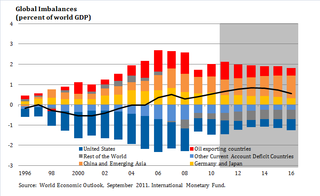

Global imbalances refers to the situation where some countries have more assets than the other countries. In theory, when the current account is in balance, it has a zero value: inflows and outflows of capital will be cancelled by each other. Hence, if the current account is persistently showing deficits for certain period, it is said to show an inequilibrium. Since, by definition, all current accounts and net foreign assets of the countries in the world must become zero, then other countries become indebted with the other nations. During recent years, global imbalances have become a concern in the rest of the world. The United States has run long term deficits, as well as many other advanced economies, while in Asia and emerging economies the opposite has occurred.

This page is based on this Wikipedia article Text is available under the CC BY-SA 4.0 license; additional terms may apply. Images, videos and audio are available under their respective licenses.