The euro is the official currency of 20 of the 27 member states of the European Union. This group of states is officially known as the euro area or, commonly, the eurozone, and includes about 344 million citizens as of 2023. The euro is divided into 100 euro cents.

The European Currency Unit was a unit of account used by the European Economic Community and composed of a basket of member country currencies. The ECU came in to operation on 13 March 1979 and was assigned the ISO 4217 code. The ECU replaced the European Unit of Account (EUA) at parity in 1979, and it was later replaced by the euro (EUR) at parity on 1 January 1999.

The Treaty on European Union, commonly known as the Maastricht Treaty, is the foundation treaty of the European Union (EU). Concluded in 1992 between the then-twelve member states of the European Communities, it announced "a new stage in the process of European integration" chiefly in provisions for a shared European citizenship, for the eventual introduction of a single currency, and for common foreign and security policies. Although these were widely seen to presage a "federal Europe", the focus of constitutional debate shifted to the later 2007 Treaty of Lisbon. In the wake of the Eurozone debt crisis unfolding from 2009, the most enduring reference to the Maastricht Treaty has been to the rules of compliance – the "Maastricht criteria" – for the currency union.

The euro area, commonly called the eurozone (EZ), is a currency union of 20 member states of the European Union (EU) that have adopted the euro (€) as their primary currency and sole legal tender, and have thus fully implemented EMU policies.

The European Exchange Rate Mechanism (ERM II) is a system introduced by the European Economic Community on 1 January 1999 alongside the introduction of a single currency, the euro as part of the European Monetary System (EMS), to reduce exchange rate variability and achieve monetary stability in Europe.

The European Monetary System (EMS) was a multilateral adjustable exchange rate agreement in which most of the nations of the European Economic Community (EEC) linked their currencies to prevent large fluctuations in relative value. It was initiated in 1979 under then President of the European Commission Roy Jenkins as an agreement among the Member States of the EEC to foster monetary policy co-operation among their Central Banks for the purpose of managing inter-community exchange rates and financing exchange market interventions.

A currency union is an intergovernmental agreement that involves two or more states sharing the same currency. These states may not necessarily have any further integration.

The euro convergence criteria are the criteria European Union member states are required to meet to enter the third stage of the Economic and Monetary Union (EMU) and adopt the euro as their currency. The four main criteria, which actually comprise five criteria as the "fiscal criterion" consists of both a "debt criterion" and a "deficit criterion", are based on Article 140 of the Treaty on the Functioning of the European Union.

Latvia replaced its previous currency, the lats, with the euro on 1 January 2014, after a European Union (EU) assessment in June 2013 asserted that the country had met all convergence criteria necessary for euro adoption. The adoption process began 1 May 2004, when Latvia joined the European Union, entering the EU's Economic and Monetary Union. At the start of 2005, the lats was pegged to the euro at Ls 0.702804 = €1, and Latvia joined the European Exchange Rate Mechanism, four months later on 2 May 2005.

Poland does not use the euro as its currency. However, under the terms of their Treaty of Accession with the European Union, all new Member States "shall participate in the Economic and Monetary Union from the date of accession as a Member State with a derogation", which means that Poland is obliged to eventually replace its currency, the złoty, with the euro.

In economics, an optimum currency area (OCA) or optimal currency region (OCR) is a geographical region in which it would maximize economic efficiency to have the entire region share a single currency.

Bulgaria plans to adopt the euro and become the 21st member state of the eurozone. The Bulgarian lev has been on the currency board since 1997 through a fixed exchange rate of the lev against the Deutsche Mark and the euro. Bulgaria's target date for introduction of the euro is 1 January 2025, which would make the euro only the second national currency of the country since the lev was introduced over 140 years ago. The official exchange rate is 1.95583 lev for 1 euro.

Romania's national currency is the leu. After Romania joined the European Union (EU) in 2007, the country became required to replace the leu with the euro once it meets all four euro convergence criteria, as stated in article 140 of the Treaty on the Functioning of the European Union. As of 2023, the only currency on the market is the leu and the euro is not yet used in shops. The Romanian leu is not part of the European Exchange Rate Mechanism, although Romanian authorities are working to prepare the changeover to the euro. To achieve the currency changeover, Romania must undergo at least two years of stability within the limits of the convergence criteria. The current Romanian government established a self-imposed criterion to reach a certain level of real convergence as a steering anchor to decide the appropriate target year for ERM II membership and Euro adoption. In March 2018, the National Plan for the Adoption of the Euro scheduled the date for euro adoption in Romania as 2024. Nevertheless, in early 2021, this date was postponed to 2027 or 2028, and once again to 2029 in late 2021 and then moved up to 2026.

Sweden does not currently use the euro as its currency and has no plans to replace the existing Swedish krona in the near future. Sweden's Treaty of Accession of 1994 made it subject to the Treaty of Maastricht, which obliges states to join the eurozone once they meet the necessary conditions. Sweden maintains that joining the European Exchange Rate Mechanism II, participation in which for at least two years is a requirement for euro adoption, is voluntary, and has chosen to remain outside pending public approval by a referendum, thereby intentionally avoiding the fulfilment of the adoption requirements.

The euro came into existence on 1 January 1999, although it had been a goal of the European Union (EU) and its predecessors since the 1960s. After tough negotiations, the Maastricht Treaty entered into force in 1993 with the goal of creating an economic and monetary union (EMU) by 1999 for all EU states except the UK and Denmark.

The United Kingdom did not seek to adopt the euro as its official currency for the duration of its membership of the European Union (EU), and secured an opt-out at the euro's creation via the Maastricht Treaty in 1992, wherein the Bank of England would only be a member of the European System of Central Banks.

Denmark uses the krone as its currency and does not use the euro, having negotiated the right to opt out from participation under the Maastricht Treaty of 1992. In 2000, the government held a referendum on introducing the euro, which was defeated with 53.2% voting no and 46.8% voting yes. The Danish krone is part of the ERM II mechanism, so its exchange rate is tied to within 2.25% of the euro.

Montenegro is a country in South-Eastern Europe, which is neither a member of the European Union (EU) nor the Eurozone; it does not have a formal monetary agreement with the EU either. However, it is one of the two territories that has unilaterally adopted the euro in 2002 as its de facto domestic currency. This means that even though the euro is not a legal tender there, it is treated as such by the government and the population.

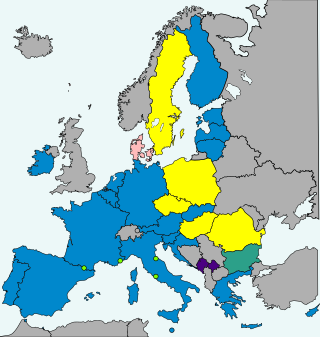

The enlargement of the eurozone is an ongoing process within the European Union (EU). All member states of the European Union, except Denmark which negotiated an opt-out from the provisions, are obliged to adopt the euro as their sole currency once they meet the criteria, which include: complying with the debt and deficit criteria outlined by the Stability and Growth Pact, keeping inflation and long-term governmental interest rates below certain reference values, stabilising their currency's exchange rate versus the euro by participating in the European Exchange Rate Mechanism, and ensuring that their national laws comply with the ECB statute, ESCB statute and articles 130+131 of the Treaty on the Functioning of the European Union. The obligation for EU member states to adopt the euro was first outlined by article 109.1j of the Maastricht Treaty of 1992, which became binding on all new member states by the terms of their treaties of accession.

The economic and monetary union (EMU) of the European Union is a group of policies aimed at converging the economies of member states of the European Union at three stages.