A landfill site, also known as a tip, dump, rubbish dump, garbage dump, or dumping ground, is a site for the disposal of waste materials. Landfill is the oldest and most common form of waste disposal, although the systematic burial of the waste with daily, intermediate and final covers only began in the 1940s. In the past, refuse was simply left in piles or thrown into pits; in archeology this is known as a midden.

The Senedd, officially known as the Welsh Parliament in English and Senedd Cymru in Welsh, is the devolved, unicameral legislature of Wales. A democratically elected body, it makes laws for Wales, agrees certain taxes and scrutinises the Welsh Government. It is a bilingual institution, with both Welsh and English being the official languages of its business. From its creation in May 1999 until May 2020, the Senedd was known as the National Assembly for Wales.

The Welsh Government is the devolved government of Wales. The government consists of ministers, who attend cabinet meetings, and deputy ministers who do not, and also of a counsel general. It is led by the first minister, usually the leader of the largest party in the Senedd, who selects ministers and deputy ministers with the approval of the Senedd. The government is responsible for tabling policy in devolved areas for consideration by the Senedd and implementing policy that has been approved by it.

Rates are a type of property tax system in the United Kingdom, and in places with systems deriving from the British one, the proceeds of which are used to fund local government. Some other countries have taxes with a more or less comparable role, like France's taxe d'habitation.

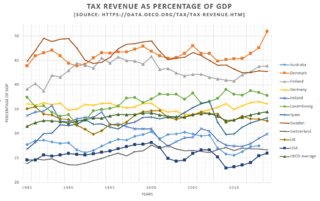

Taxation in the United Kingdom may involve payments to at least three different levels of government: central government, devolved governments and local government. Central government revenues come primarily from income tax, National Insurance contributions, value added tax, corporation tax and fuel duty. Local government revenues come primarily from grants from central government funds, business rates in England, Council Tax and increasingly from fees and charges such as those for on-street parking. In the fiscal year 2014–15, total government revenue was forecast to be £648 billion, or 37.7 per cent of GDP, with net taxes and National Insurance contributions standing at £606 billion.

Income taxes are the most significant form of taxation in Australia, and collected by the federal government through the Australian Taxation Office. Australian GST revenue is collected by the Federal government, and then paid to the states under a distribution formula determined by the Commonwealth Grants Commission.

Business rates in England, or non-domestic rates, are a tax on the occupation of non-domestic property. Rates are a property tax with ancient roots that was formerly used to fund local services that was formalised with the Poor Law 1572 and superseded by the Poor Law of 1601. The Local Government Finance Act 1988 introduced business rates in England and Wales from 1990, repealing its immediate predecessor, the General Rate Act 1967. The act also introduced business rates in Scotland but as an amendment to the existing system, which had evolved separately to that in the rest of Great Britain. Since the establishment in 1997 of a Welsh Assembly able to pass legislation, the English and Welsh systems have been able to diverge. In 2015, business rates for Wales were devolved.

A landfill tax or levy is a form of tax that is applied in some countries to increase the cost of landfill. The tax is typically levied in units of currency per unit of weight or volume. The tax is in addition to the overall cost of landfill and forms a proportion of the gate fee.

In 2015, 43.5% of the United Kingdom's municipal waste was recycled, composted or broken down by anaerobic digestion. The majority of recycling undertaken in the United Kingdom is done by statutory authorities, although commercial and industrial waste is chiefly processed by private companies. Local Authorities are responsible for the collection of municipal waste and operate contracts which are usually kerbside collection schemes. The Household Waste Recycling Act 2003 required local authorities in England to provide every household with a separate collection of at least two types of recyclable materials by 2010. Recycling policy is devolved to the administrations of Scotland, Northern Ireland and Wales who set their own targets, but all statistics are reported to Eurostat.

Waste management laws govern the transport, treatment, storage, and disposal of all manner of waste, including municipal solid waste, hazardous waste, and nuclear waste, among many other types. Waste laws are generally designed to minimize or eliminate the uncontrolled dispersal of waste materials into the environment in a manner that may cause ecological or biological harm, and include laws designed to reduce the generation of waste and promote or mandate waste recycling. Regulatory efforts include identifying and categorizing waste types and mandating transport, treatment, storage, and disposal practices.

The Office for Budget Responsibility (OBR) is a non-departmental public body funded by the UK Treasury, that the UK government established to provide independent economic forecasts and independent analysis of the public finances. It was formally created in May 2010 following the general election and was placed on a statutory footing by the Budget Responsibility and National Audit Act 2011. It is one of a growing number of official independent fiscal watchdogs around the world.

Taxation may involve payments to a minimum of two different levels of government: central government through SARS or to local government. Prior to 2001 the South African tax system was "source-based", where in income is taxed in the country where it originates. Since January 2001, the tax system was changed to "residence-based" wherein taxpayers residing in South Africa are taxed on their income irrespective of its source. Non residents are only subject to domestic taxes.

The Wales Act 2014 is an Act of the Parliament of the United Kingdom.

The Landfill Tax (Scotland) Act 2014 is an Act of the Scottish Parliament, introduced to the legislature in 2013 and receiving Royal Assent on 21 January 2014, which creates a new Scottish Landfill Tax. The tax applies mainly to waste management companies and local authorities disposing of waste at landfill.

The Welsh Revenue Authority is a non-ministerial department of the Welsh Government responsible for the administration and collection of devolved taxes in Wales.

Welsh Rates of Income Tax (WRIT) is part of the UK income tax system and from 6 April 2019 a proportion of income tax paid by taxpayers living in Wales is transferred straight to the Welsh Government to fund Welsh public services. It is administered by HM Revenue and Customs (HMRC), but it is not a devolved tax comparable to Scottish income tax.

Waste management in Australia started to be implemented as a modern system by the second half of the 19th century, with its progresses driven by technological and sanitary advances. It is currently regulated at both federal and state level. The Commonwealth's Department of the Environment and Energy is responsible for the national legislative framework.

Taxation in Wales typically comprises payments to one or more of the three different levels of government: the UK government, the Welsh Government, and local government.

Land Transaction Tax (LTT) is a property tax in Wales. It replaced the Stamp Duty Land Tax from 1 April 2018. It became the first Welsh tax in almost 800 years.

The Welsh fiscal balance is the difference between general government revenues and expenditures, showing how much in a given year government spending is financed by the revenues collected in Wales.