Related Research Articles

Microeconomics is a branch of mainstream economics that studies the behavior of individuals and firms in making decisions regarding the allocation of scarce resources and the interactions among these individuals and firms. Microeconomics focuses on the study of individual markets, sectors, or industries as opposed to the national economy as whole, which is studied in macroeconomics.

A monopoly, as described by Irving Fisher, is a market with the "absence of competition", creating a situation where a specific person or enterprise is the only supplier of a particular thing. This contrasts with a monopsony which relates to a single entity's control of a market to purchase a good or service, and with oligopoly and duopoly which consists of a few sellers dominating a market. Monopolies are thus characterised by a lack of economic competition to produce the good or service, a lack of viable substitute goods, and the possibility of a high monopoly price well above the seller's marginal cost that leads to a high monopoly profit. The verb monopolise or monopolize refers to the process by which a company gains the ability to raise prices or exclude competitors. In economics, a monopoly is a single seller. In law, a monopoly is a business entity that has significant market power, that is, the power to charge overly high prices, which is associated with a decrease in social surplus. Although monopolies may be big businesses, size is not a characteristic of a monopoly. A small business may still have the power to raise prices in a small industry.

Monopolistic competition is a type of imperfect competition such that there are many producers competing against each other, but selling products that are differentiated from one another and hence are not perfect substitutes. In monopolistic competition, a company takes the prices charged by its rivals as given and ignores the impact of its own prices on the prices of other companies. If this happens in the presence of a coercive government, monopolistic competition will fall into government-granted monopoly. Unlike perfect competition, the company maintains spare capacity. Models of monopolistic competition are often used to model industries. Textbook examples of industries with market structures similar to monopolistic competition include restaurants, cereals, clothing, shoes, and service industries in large cities. The "founding father" of the theory of monopolistic competition is Edward Hastings Chamberlin, who wrote a pioneering book on the subject, Theory of Monopolistic Competition (1933). Joan Robinson published a book The Economics of Imperfect Competition with a comparable theme of distinguishing perfect from imperfect competition. Further work on monopolistic competition was undertaken by Dixit and Stiglitz who created the Dixit-Stiglitz model which has proved applicable used in the sub fields of international trade theory, macroeconomics and economic geography.

An oligopoly is a market structure in which a market or industry is dominated by a small number of large sellers or producers. Oligopolies often result from the desire to maximize profits, which can lead to collusion between companies. This reduces competition, increases prices for consumers, and lowers wages for employees.

In microeconomics, supply and demand is an economic model of price determination in a market. It postulates that, holding all else equal, in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded will equal the quantity supplied, resulting in an economic equilibrium for price and quantity transacted. The concept of supply and demand forms the theoretical basis of modern economics.

In economics, imperfect competition refers to a situation where the characteristics of an economic market do not fulfil all the necessary conditions of a perfectly competitive market. Imperfect competition will cause market inefficiency when it happens, resulting in market failure. Imperfect competition is a term usually used to describe the seller's position, meaning that the level of competition between sellers falls far short of the level of competition in the market under ideal conditions.

This aims to be a complete article list of economics topics:

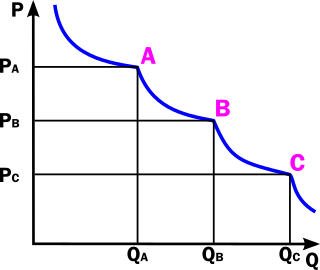

Price discrimination is a microeconomic pricing strategy where identical or largely similar goods or services are sold at different prices by the same provider in different market segments. Price discrimination is distinguished from product differentiation by the more substantial difference in production cost for the differently priced products involved in the latter strategy. Price differentiation essentially relies on the variation in the customers' willingness to pay and in the elasticity of their demand. For price discrimination to succeed, a firm must have market power, such as a dominant market share, product uniqueness, sole pricing power, etc. All prices under price discrimination are higher than the equilibrium price in a perfectly-competitive market. However, some prices under price discrimination may be lower than the price charged by a single-price monopolist.

A good's price elasticity of demand is a measure of how sensitive the quantity demanded is to its price. When the price rises, quantity demanded falls for almost any good, but it falls more for some than for others. The price elasticity gives the percentage change in quantity demanded when there is a one percent increase in price, holding everything else constant. If the elasticity is −2, that means a one percent price rise leads to a two percent decline in quantity demanded. Other elasticities measure how the quantity demanded changes with other variables.

In economics, the cross elasticity of demand or cross-price elasticity of demand measures the percentage change of the quantity demanded for a good to the percentage change in the price of another good, ceteris paribus. In real life, the quantity demanded of good is dependent on not only its own price but also the price of other "related" products.

Price points are prices at which demand for a given product is supposed to stay relatively high.

Monopoly profit is an inflated level of profit due to the monopolistic practices of an enterprise.

In microeconomics, the law of demand is a fundamental principle which states that there is an inverse relationship between price and quantity demanded. In other words, "conditional on all else being equal, as the price of a good increases (↑), quantity demanded will decrease (↓); conversely, as the price of a good decreases (↓), quantity demanded will increase (↑)". Alfred Marshall worded this as: "When we say that a person's demand for anything increases, we mean that he will buy more of it than he would before at the same price, and that he will buy as much of it as before at a higher price". The law of demand, however, only makes a qualitative statement in the sense that it describes the direction of change in the amount of quantity demanded but not the magnitude of change.

In economics, market power refers to the ability of a firm to influence the price at which it sells a product or service by manipulating either the supply or demand of the product or service to increase economic profit. In other words, market power occurs if a firm does not face a perfectly elastic demand curve and can set its price (P) above marginal cost (MC) without losing revenue. This indicates that the magnitude of market power is associated with the gap between P and MC at a firm's profit maximising level of output. Such propensities contradict perfectly competitive markets, where market participants have no market power, P = MC and firms earn zero economic profit. Market participants in perfectly competitive markets are consequently referred to as 'price takers', whereas market participants that exhibit market power are referred to as 'price makers' or 'price setters'.

Market structure, in economics, depicts how firms are differentiated and categorised based on the types of goods they sell (homogeneous/heterogeneous) and how their operations are affected by external factors and elements. Market structure makes it easier to understand the characteristics of diverse markets.

In economics, tax incidence or tax burden is the effect of a particular tax on the distribution of economic welfare. Economists distinguish between the entities who ultimately bear the tax burden and those on whom the tax is initially imposed. The tax burden measures the true economic effect of the tax, measured by the difference between real incomes or utilities before and after imposing the tax, and taking into account how the tax causes prices to change. For example, if a 10% tax is imposed on sellers of butter, but the market price rises 8% as a result, most of the tax burden is on buyers, not sellers. The concept of tax incidence was initially brought to economists' attention by the French Physiocrats, in particular François Quesnay, who argued that the incidence of all taxation falls ultimately on landowners and is at the expense of land rent. Tax incidence is said to "fall" upon the group that ultimately bears the burden of, or ultimately suffers a loss from, the tax. The key concept of tax incidence is that the tax incidence or tax burden does not depend on where the revenue is collected, but on the price elasticity of demand and price elasticity of supply. As a general policy matter, the tax incidence should not violate the principles of a desirable tax system, especially fairness and transparency. The concept of tax incidence is used in political science and sociology to analyze the level of resources extracted from each income social stratum in order to describe how the tax burden is distributed among social classes. That allows one to derive some inferences about the progressive nature of the tax system, according to principles of vertical equity.

In economics, partial equilibrium is a condition of economic equilibrium which analyzes only a single market, ceteris paribus except for the one change at a time being analyzed. In general equilibrium analysis, on the other hand, the prices and quantities of all markets in the economy are considered simultaneously, including feedback effects from one to another, though the assumption of ceteris paribus is maintained with respect to such things as constancy of tastes and technology.

In competition law, before deciding whether companies have significant market power which would justify government intervention, the test of small but significant and non-transitory increase in price (SSNIP) is used to define the relevant market in a consistent way. It is an alternative to ad hoc determination of the relevant market by arguments about product similarity.

In economics, profit is the difference between revenue that an economic entity has received from its outputs and total costs of its inputs. It is equal to total revenue minus total cost, including both explicit and implicit costs.

The following outline is provided as an overview of and topical guide to economics:

References

- ↑ Monroe E. Price, Television: The Public Sphere and National Identity 67 (1995); Monroe E. Price, Law, Force and the Russian Media, 13 Cardozo Arts & Ent. L.J. 795 (1995); Monroe E. Price, The Market for Loyalties and the Uses of Comparative Media Law, in Broadcasting Reform in India: Media Law from A Global Perspective 93 (Monroe E. Price & Stefaan G. Verhulst Eds., 1998); Monroe E. Price, Media and Sovereignty: The Global Information Revolution and its Challenge to State Power 32 (2002); Monroe E. Price, The Market for Loyalties: Electronic Media and the Global Competition for Allegiances, 104 Yale L.J. 667 (1994); Monroe E. Price, The Market for Loyalties and the Uses of "Comparative Media Law", 5 Cardozo J. Int’l & Comp. L. 445 (1997); Monroe E. Price, The Newness of New Technologies, 22 Cardozo L. Rev. 1885 (2001).

- ↑ Monroe E. Price, Market for Loyalties: Electronic Media and the Global Competition for Allegiances, 104 Yale L.J., at 669.

- ↑ Id., at 669-70.

- ↑ Paul D. Callister, Identity and Market for Loyalties Theories: The Case for Free Information Flow in Insurgent Iraq, 25 St.Louis U.Pub.L.Rev. 124, 136 (2006)

- ↑ Douglas A.L. Auld et al., American Dictionary of Economics 306 (1983) (under entry for Substitutes).

- ↑ Marco Fanno, The Elasticity of Demand of Substitute Goods, 3 Italian Econ. Papers 99, 115 (1998). This article is a translation of an article originally published in German as: Marco Fanno, Die Elastizität der Nachfrage nach Ersatzgütern, in Zeitscrift fϋr Nationalökonomie 51 (1930). The German article was meant to be a synthesis of a much longer Fanno essay that was earlier published in Italian: Marco Fanno, Contributo alla Teoria Economica dei Beni Succedanei, in 2 Annali di Economia 331 (1925-26).

- ↑ See Callister supra, note 4, at 153; Paul D. Callister, The Internet, Regulation and the Market for Loyalties: An Economic Analysis of Transborder Information Flow, 2002 Journal of Law, Technology and Policy 59,90-103.

- ↑ See Callister supra note 4 at 139-40.

- ↑ See id. supra note 4 at 140-45.

- ↑ See id. supra note 4 at 146.

- ↑ See Paul D. Callister & Kimberlee Everson, Analysis of Freedom of Information for its Effect on Society by Considering 2011, the Year of the Arab Spring, 6 Information Law Journal 36 (2015).