In the United States, a 401(k) plan is an employer-sponsored, defined-contribution, personal pension (savings) account, as defined in subsection 401(k) of the U.S. Internal Revenue Code. Periodic employee contributions come directly out of their paychecks, and may be matched by the employer. This legal option is what makes 401(k) plans attractive to employees, and many employers offer this option to their (full-time) workers. 401(k) payable is a general ledger account that contains the amount of 401(k) plan pension payments that an employer has an obligation to remit to a pension plan administrator. This account is classified as a payroll liability, since the amount owed should be paid within one year.

A pension is a fund into which amounts are paid regularly during an individual's working career, and from which periodic payments are made to support the person's retirement from work. A pension may be:

In the United States, Social Security is the commonly used term for the federal Old-Age, Survivors, and Disability Insurance (OASDI) program and is administered by the Social Security Administration (SSA). The Social Security Act was passed in 1935, and the existing version of the Act, as amended, encompasses several social welfare and social insurance programs.

The Federal Old-Age and Survivors Insurance Trust Fund and Federal Disability Insurance Trust Fund are trust funds that provide for payment of Social Security benefits administered by the United States Social Security Administration.

The Canada Pension Plan is a contributory, earnings-related social insurance program. It forms one of the two major components of Canada's public retirement income system, the other component being Old Age Security (OAS). Other parts of Canada's retirement system are private pensions, either employer-sponsored or from tax-deferred individual savings. As of June 30, 2022, the CPP Investment Board manages over C$523 billion in investment assets for the Canada Pension Plan on behalf of 21 million Canadians. CPPIB is one of the world's biggest pension funds.

A retirement plan is a financial arrangement designed to replace employment income upon retirement. These plans may be set up by employers, insurance companies, trade unions, the government, or other institutions. Congress has expressed a desire to encourage responsible retirement planning by granting favorable tax treatment to a wide variety of plans. Federal tax aspects of retirement plans in the United States are based on provisions of the Internal Revenue Code and the plans are regulated by the Department of Labor under the provisions of the Employee Retirement Income Security Act (ERISA).

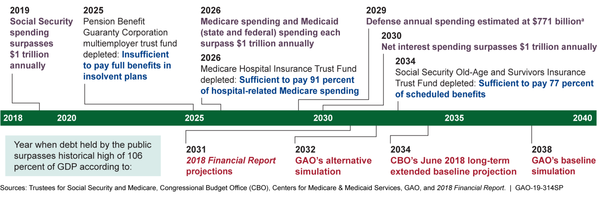

The Social Security debate in the United States encompasses benefits, funding, and other issues. xSocial Security is a social insurance program officially called "Old-age, Survivors, and Disability Insurance" (OASDI), in reference to its three components. It is primarily funded through a dedicated payroll tax. During 2015, total benefits of $897 billion were paid out versus $920 billion in income, a $23 billion annual surplus. Excluding interest of $93 billion, the program had a cash deficit of $70 billion. Social Security represents approximately 40% of the income of the elderly, with 53% of married couples and 74% of unmarried persons receiving 50% or more of their income from the program. An estimated 169 million people paid into the program and 60 million received benefits in 2015, roughly 2.82 workers per beneficiary. Reform proposals continue to circulate with some urgency, due to a long-term funding challenge faced by the program as the ratio of workers to beneficiaries falls, driven by the aging of the baby-boom generation, expected continuing low birth rate, and increasing life expectancy. Program payouts began exceeding cash program revenues in 2011; this shortfall is expected to continue indefinitely under current law.

The Pension Benefit Guaranty Corporation (PBGC) is a United States federally chartered corporation created by the Employee Retirement Income Security Act of 1974 (ERISA) to encourage the continuation and maintenance of voluntary private defined benefit pension plans, provide timely and uninterrupted payment of pension benefits, and keep pension insurance premiums at the lowest level necessary to carry out its operations. Subject to other statutory limitations, PBGC's single-employer insurance program pays pension benefits up to the maximum guaranteed benefit set by law to participants who retire at 65. The benefits payable to insured retirees who start their benefits at ages other than 65 or elect survivor coverage are adjusted to be equivalent in value. The maximum monthly guarantee for the multiemployer program is far lower and more complicated.

Superannuation in Australia or "super" is a savings system for workplace pensions in retirement. It involves money earned by an employee being placed into an investment fund to be made legally available to fund members upon retirement. Employers make compulsory payments to these funds at a proportion of their employee's wages. From July 2023, the mandatory minimum "guarantee" contribution is 11%, rising to 12% from 2025. The superannuation guarantee was introduced by the Hawke government to promote self-funded retirement savings, reducing reliance on a publicly funded pension system. Legislation to support the introduction of the superannuation guarantee was passed by the Keating Government in 1992.

A defined contribution (DC) plan is a type of retirement plan in which the employer, employee or both make contributions on a regular basis. Individual accounts are set up for participants and benefits are based on the amounts credited to these accounts plus any investment earnings on the money in the account. In defined contribution plans, future benefits fluctuate on the basis of investment earnings. The most common type of defined contribution plan is a savings and thrift plan. Under this type of plan, the employee contributes a predetermined portion of his or her earnings to an individual account, all or part of which is matched by the employer.

Pensions in the United States consist of the Social Security system, public employees retirement systems, as well as various private pension plans offered by employers, insurance companies, and unions.

A private pension is a plan into which individuals privately contribute from their earnings, which then will pay them a pension after retirement. It is an alternative to the state pension. Usually, individuals invest funds into saving schemes or mutual funds, run by insurance companies. Often private pensions are also run by the employer and are called occupational pensions. The contributions into private pension schemes are usually tax-deductible.

In the United States, public sector pensions are offered at the federal, state, and local levels of government. They are available to most, but not all, public sector employees. These employer contributions to these plans typically vest after some period of time, e.g. 5 years of service. These plans may be defined-benefit or defined-contribution pension plans, but the former have been most widely used by public agencies in the U.S. throughout the late twentieth century. Some local governments do not offer defined-benefit pensions but may offer a defined contribution plan. In many states, public employee pension plans are known as Public Employee Retirement Systems (PERS).

The Public Employees Retirement System (PERS) is the retirement and disability fund for public employees in the U.S. state of Oregon established in 1946. Employees of the state, school districts, and local governments are eligible for coverage. A health insurance plan for covered retirees was added to the program in 1987. The program is administered by a twelve-member board of trustees, appointed to three-year terms by the Governor subject to confirmation by the Senate, which also administers the Oregon Savings Growth Plan, a voluntary deferred compensation plan established in 1991.

Defined benefit (DB) pension plan is a type of pension plan in which an employer/sponsor promises a specified pension payment, lump-sum, or combination thereof on retirement that depends on an employee's earnings history, tenure of service and age, rather than depending directly on individual investment returns. Traditionally, many governmental and public entities, as well as a large number of corporations, provide defined benefit plans, sometimes as a means of compensating workers in lieu of increased pay.

At retirement, individuals stop working and no longer get employment earnings, and enter a phase of their lives, where they rely on the assets they have accumulated, to supply money for their spending needs for the rest of their lives. Retirement spend-down, or withdrawal rate, is the strategy a retiree follows to spend, decumulate or withdraw assets during retirement.

In France, pensions fall into five major divisions;

Pensions in Spain consist of a mandatory state pension scheme, and voluntary company and individual pension provision.

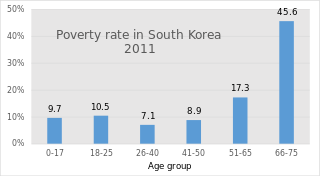

South Korea's pension scheme was introduced relatively recently, compared to other democratic nations. Half of the country's population aged 65 and over lives in relative poverty, or nearly four times the 13% average for member countries of the Organisation for Economic Co-operation and Development (OECD). This makes old age poverty an urgent social problem. Public social spending by general government is half the OECD average, and is the lowest as a percentage of GDP among OECD member countries.

The Illinois pension crisis refers to the rising gap between the pension benefits owed to eligible state employees and the amount of funding set aside by the state to make these future pension payments. As of 2020, the size of Illinois' pension obligation is $237B, but the state's pension funds have only $96B available for payouts to retirees.