Related Research Articles

In the United States, a 401(k) plan is an employer-sponsored, defined-contribution, personal pension (savings) account, as defined in subsection 401(k) of the U.S. Internal Revenue Code. Periodic employee contributions come directly out of their paychecks, and may be matched by the employer. This legal option is what makes 401(k) plans attractive to employees, and many employers offer this option to their (full-time) workers. 401(k) payable is a general ledger account that contains the amount of 401(k) plan pension payments that an employer has an obligation to remit to a pension plan administrator. This account is classified as a payroll liability, since the amount owed should be paid within one year.

A pension is a fund into which amounts are paid regularly during the individual's working career, and from which periodic payments are made to support the person's retirement from work. A pension may be:

A pension fund, also known as a superannuation fund in some countries, is any program, fund, or scheme which provides retirement income.

The Central Provident Fund Board (CPFB), commonly known as the CPF Board or simply the Central Provident Fund (CPF), is a compulsory comprehensive savings and pension plan for working Singaporeans and permanent residents primarily to fund their retirement, healthcare, education and housing needs in Singapore.

The Employees' Provident Fund Organisation (EPFO) is one of the two main social security organization under the Government of India's Ministry of Labour and Employment and is responsible for regulation and management of provident funds in India, the other being Employees' State Insurance. The EPFO administers the mandatory provident fund, a basic pension scheme and a disability/death insurance scheme. It also manages social security agreements with other countries. International workers are covered under EPFO plans in countries where bilateral agreements have been signed. As of May 2021, 19 such agreements are in place. The EPFO's top decision-making body is the Central Board of Trustees (CBT), a statutory body established by the Employees' Provident Fund and Miscellaneous Provisions (EPF&MP) Act, 1952. As of 2018, more than ₹11 lakh crore are under EPFO management.

Pensions in the United Kingdom, whereby United Kingdom tax payers have some of their wages deducted to save for retirement, can be categorised into three major divisions - state, occupational and personal pensions.

In Australia, superannuation or "super" is a retirement savings system. It involves money earned by an employee being placed into an investment fund to be made legally available to fund members upon retirement.

A defined contribution (DC) plan is a type of retirement plan in which the employer, employee or both make contributions on a regular basis. Individual accounts are set up for participants and benefits are based on the amounts credited to these accounts plus any investment earnings on the money in the account. In defined contribution plans, future benefits fluctuate on the basis of investment earnings. The most common type of defined contribution plan is a savings and thrift plan. Under this type of plan, the employee contributes a predetermined portion of his or her earnings to an individual account, all or part of which is matched by the employer.

The Mandatory Provident Fund, often abbreviated as MPF (強積金), is a compulsory saving scheme for the retirement of residents in Hong Kong. Most employees and their employers are required to contribute monthly to mandatory provident fund schemes provided by approved private organisations, according to their salaries and the period of employment.

A private pension is a plan into which individuals contribute from their earnings, which then will pay them a private pension after retirement. It is an alternative to the state pension. Usually, individuals invest funds into saving schemes or mutual funds, run by insurance companies. Often private pensions are also run by the employer and are called occupational pensions. The contributions into private pension schemes are usually tax-deductible. This is similar to the regular pension.

Provident fund is another name for pension fund. Its purpose is to provide employees with lump sum payments at the time of exit from their place of employment. This differs from pension funds, which have elements of both lump sum as well as monthly pension payments. As far as differences between gratuity and provident funds are concerned, although both types involve lump sum payments at the end of employment, the former operates as a defined benefit plan, while the latter is a defined contribution plan.

Social security in India includes a variety of statutory insurances and social grant schemes bundled into a formerly complex and fragmented system run by the Indian government at the federal and the state level. The Directive Principles of State Policy, enshrined in Part IV of the Indian Constitution reflects that India is a welfare state. Food security to all Indians are guaranteed under the National Food Security Act, 2013 where the government provides highly subsidised food grains or a food security allowance to economically vulnerable people. The system has since been universalised with the passing of The Code on Social Security, 2020. These cover most of the Indian population with social protection in various situations in their lives.

A Personal Retirement Savings Account (PRSA) is a type of savings account introduced to the Irish market in 2003. In an attempt to increase pension coverage, the Pensions Board introduced a retirement savings account, that would entice the lower paid and self-employed to start making some pension provision. The intention was for PRSAs to supplement any State Retirement Benefits that would be payable in years to come.

The National Pension System (NPS) is a defined-contribution pension system in India regulated by Pension Fund Regulatory and Development Authority (PFRDA) which is under the jurisdiction of Ministry of Finance of the Government of India. National Pension System Trust was established by PFRDA as per the provisions of the Indian Trusts Act of 1882 for taking care of the assets and funds under this scheme for the best interest of the subscriber.

Defined benefit (DB) pension plan is a type of pension plan in which an employer/sponsor promises a specified pension payment, lump-sum, or combination thereof on retirement that depends on an employee's earnings history, tenure of service and age, rather than depending directly on individual investment returns. Traditionally, many governmental and public entities, as well as a large number of corporations, provide defined benefit plans, sometimes as a means of compensating workers in lieu of increased pay.

In France, pensions fall into five major divisions;

Pensions in Germany are based on a “three pillar system”.

There are various types of Pensions in Armenia, including social pensions, mandatory funded pensions, or voluntary funded pensions. Currently, Amundi-ACBA and Ampega act as the mandatory pension fund managers within Armenia.

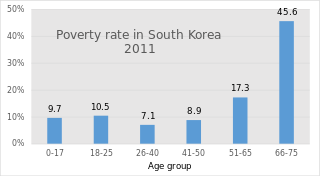

South Korea's pension scheme was introduced relatively recently, compared to other democratic nations. Half of the country's population aged 65 and over lives in relative poverty, or nearly four times the 13% average for member countries of the Organisation for Economic Co-operation and Development (OECD). This makes old age poverty an urgent social problem. Public social spending by general government is half the OECD average, and is the lowest as a percentage of GDP among OECD member countries.

Pensions in Denmark consist of both private and public programs, all managed by the Agency for the Modernisation of Public Administration under the Ministry of Finance. Denmark created a multipillar system, consisting of an unfunded social pension scheme, occupational pensions, and voluntary personal pension plans. Denmark's system is a close resemblance to that encouraged by the World Bank in 1994, emphasizing the international importance of establishing multifaceted pension systems based on public old-age benefit plans to cover the basic needs of the elderly. The Danish system employed a flat-rate benefit funded by the government budget and available to all Danish residents. The employment-based contribution plans are negotiated between employers and employees at the individual firm or profession level, and cover individuals by labor market systems. These plans have emerged as a result of the centralized wage agreements and company policies guaranteeing minimum rates of interest. The last pillar of the Danish pension system is income derived from tax-subsidized personal pension plans, established with life insurance companies and banks. Personal pensions are inspired by tax considerations, desirable to people not covered by the occupational scheme.

References

- ↑ India Social Pension Archived 2012-05-01 at the Wayback Machine . GlobalAging.org. Accessed April 29, 2012.

- ↑ "National Social Assistance Programme (NSAP)|Ministry Of Rural Development|Government Of India". NSAP. Retrieved 11 August 2022.

- ↑ "Govt to scrap pension scheme for new staff - Times of India". The Times of India . 16 October 2003.

- ↑ https://www.policybazaar.com/life-insurance/pension-plans/articles/how-general-provident-funds-works/ [ bare URL ]

- ↑ "EPFO || For Employees". Epfindia.gov.in. Retrieved 11 August 2022.

- ↑ "Retirement Planning: How much money do you need to retire comfortably in India?".

- ↑ {{citation |title=Good News! Unorganised workers can now subscribe to this pension scheme |url=https://www.shaleshyadav.com/2020/07/sspy-sspy-pension-list-2020-sarkari.html?m=1%7Cwork=[[government pension yojna}}