Related Research Articles

A pension is a fund into which amounts are paid regularly during an individual's working career, and from which periodic payments are made to support the person's retirement from work. A pension may be:

In the United States, Social Security is the commonly used term for the federal Old-Age, Survivors, and Disability Insurance (OASDI) program and is administered by the Social Security Administration (SSA). The Social Security Act was passed in 1935, and the existing version of the Act, as amended, encompasses several social welfare and social insurance programs.

Medicare is a government national health insurance program in the United States, begun in 1965 under the Social Security Administration (SSA) and now administered by the Centers for Medicare and Medicaid Services (CMS). It primarily provides health insurance for Americans aged 65 and older, but also for some younger people with disability status as determined by the SSA, including people with end stage renal disease and amyotrophic lateral sclerosis.

Supplemental Security Income (SSI) is a means-tested program that provides cash payments to disabled children, disabled adults, and individuals aged 65 or older who are citizens or nationals of the United States. SSI was created by the Social Security Amendments of 1972 and is incorporated in Title 16 of the Social Security Act. The program is administered by the Social Security Administration (SSA) and began operations in 1974.

The United States Social Security Administration (SSA) is an independent agency of the U.S. federal government that administers Social Security, a social insurance program consisting of retirement, disability and survivor benefits. To qualify for most of these benefits, most workers pay Social Security taxes on their earnings; the claimant's benefits are based on the wage earner's contributions. Otherwise benefits such as Supplemental Security Income (SSI) are given based on need.

The Federal Insurance Contributions Act is a United States federal payroll contribution directed towards both employees and employers to fund Social Security and Medicare—federal programs that provide benefits for retirees, people with disabilities, and children of deceased workers.

A disability pension is a form of pension given to those people who are permanently or temporarily unable to work due to a disability.

Term life insurance or term assurance is life insurance that provides coverage at a fixed rate of payments for a limited period of time, the relevant term. After that period expires, coverage at the previous rate of premiums is no longer guaranteed and the client must either forgo coverage or potentially obtain further coverage with different payments or conditions. If the life insured dies during the term, the death benefit will be paid to the beneficiary. Term insurance is typically the least expensive way to purchase a substantial death benefit on a coverage amount per premium dollar basis over a specific period of time.

The Federal Employees' Retirement System (FERS) is the retirement system for employees within the United States civil service. FERS became effective January 1, 1987, to replace the Civil Service Retirement System (CSRS) and to conform federal retirement plans in line with those in the private sector.

Social Security Disability Insurance is a payroll tax-funded federal insurance program of the United States government. It is managed by the Social Security Administration and designed to provide monthly benefits to people who have a medically determinable disability that restricts their ability to be employed. SSDI does not provide partial or temporary benefits but rather pays only full benefits and only pays benefits in cases in which the disability is "expected to last at least one year or result in death." Relative to disability programs in other countries in the Organisation for Economic Co-operation and Development (OECD), the SSDI program in the United States has strict requirements regarding eligibility.

Under the United States social security system, workers who have reached 62 but have not yet reached the full social security retirement age are subject to a retirement earnings test, which effectively defers benefits for people whose earnings are above a given threshold.

The Windfall Elimination Provision is a statutory provision in United States law which affects benefits paid by the Social Security Administration under Title II of the Social Security Act. It reduces the Primary Insurance Amount (PIA) of a person's Retirement Insurance Benefits (RIB) or Disability Insurance Benefits (DIB) when that person is eligible or entitled to a pension based on a job which did not contribute to the Social Security Trust Fund. While in effect, it also affects the benefits of others claiming on the same social security record.

Years of coverage, for purposes of the American Social Security program, are years in which a beneficiary is considered to have contributed a substantial amount into the Social Security Trust Fund. Years of coverage are used in the computations in whether and how to apply the Windfall Elimination Provision. Years of coverage are not the amounts used in similar computations, such as with Quarter Credits.

The Primary Insurance Amount (PIA) is a component of Social Security provision in the United States. Eligibility for receiving Social Security benefits, for all persons born after 1929, requires accumulating a minimum of 40 Social Security credits. Typically this is accomplished by earning income from work on which Federal Insurance Contributions Act (FICA) tax is assessed, up to a maximum taxable earnings threshold. For the purposes of the United States Social Security Administration, PIA is used as the beginning point in calculating the annuity payment of benefits that is provided to an eligible recipient each month during retirement until the recipient's death. Generally, the more a person pays in FICA taxes during their life, the higher their PIA will be. However, specific rules in its computation may deviate from this general rule.

Disability benefits are funds provided from public or private sources to a person who is ill or who has a disability.

The Social Security Organization (SSO) is a social insurance organization in Iran which provides coverage of wage-earners and salaried workers as well as voluntary coverage of self-employed persons. In 1975, the laws Social Security Law was approved and the SSO was established.

In France, pensions fall into five major divisions;

The National Social Assistance Programme (NSAP) is a Centrally Sponsored Scheme of the Government of India that provides financial assistance to the elderly, widows and persons with disabilities in the form of social pensions. The NSAP scheme only includes Below Poverty Line individuals as beneficiaries.

The Government Pension Offset (GPO) is a statutory provision in United States law which affects benefits paid by the Social Security Administration. It reduces spousal Social Security retirement benefits in situations where the spouse did not pay Social Security taxes on their employment earnings. One exception to this provision occurs when the spouse is receiving a foreign pension for a different country, in which case the Government Pension Offset is not applied. This is in contrast to the Windfall Elimination Provision (WEP), which reduces Social Security benefits of the actual number holder on whose Social Security record the claim is filed.

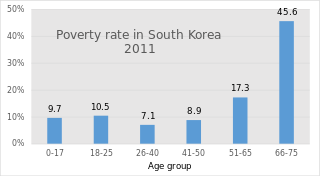

South Korea's pension scheme was introduced relatively recently, compared to other democratic nations. Half of the country's population aged 65 and over lives in relative poverty, or nearly four times the 13% average for member countries of the Organisation for Economic Co-operation and Development (OECD). This makes old age poverty an urgent social problem. Public social spending by general government is half the OECD average, and is the lowest as a percentage of GDP among OECD member countries.

References

- ↑ http://www.ssa.gov/glossary.htm#R

- 1 2 Social Security Act Title II § 202

- 1 2 POMS RS 00201.001

- 1 2 "POMS RS 00301.105". Social Security Administration .

- ↑ "Quarters of Coverage". Social Security Administration. Retrieved August 12, 2020.

- ↑ POMS RS 00615.015

- ↑ "Social Security Office Locator, SSA Office Locator Social Security Office Locator, Social Security".

- ↑ "Apply for Social Security Benefits | SSA".

- ↑ POMS RS 00605.001

- ↑ POMS RS 00615.101

- 1 2 3 https://www.ssa.gov/pubs/EN-05-10147.pdf [ bare URL PDF ]

- ↑ POMS RS 00615.690

- ↑ POMS RS 02501.001

- ↑ "The President Signs the "Senior Citizens' Freedom to Work Act of 2000"".

- 1 2 POMS RS 02501.021

- ↑ "Exempt Amounts Under the Earnings Test".

- 1 2 https://www.ssa.gov/pubs/EN-05-10069.pdf [ bare URL PDF ]

- ↑ POMS RS 02501.030

- ↑ POMS RS 02505.065

- ↑ POMS RS 02501.025

- ↑ POMS RS 00605.360

- ↑ POMS RS 00605.362

- ↑ POMS RS 00615.003

- ↑ POMS GN 02401.001

- ↑ POMS GN 02407.005

- ↑ POMS RS 00201.002