Finance is the study and discipline of money, currency and capital assets. It is related to and distinct from Economics which is the study of production, distribution, and consumption of goods and services. The discipline of Financial Economics bridges the two fields. Based on the scope of financial activities in financial systems, the discipline can be divided into personal, corporate, and public finance.

An interest rate is the amount of interest due per period, as a proportion of the amount lent, deposited, or borrowed. The total interest on an amount lent or borrowed depends on the principal sum, the interest rate, the compounding frequency, and the length of time over which it is lent, deposited, or borrowed.

Personal finance is the financial management that an individual or a family unit performs to budget, save, and spend monetary resources over time, taking into account various financial risks and future life events.

Capital accumulation is the dynamic that motivates the pursuit of profit, involving the investment of money or any financial asset with the goal of increasing the initial monetary value of said asset as a financial return whether in the form of profit, rent, interest, royalties or capital gains. The aim of capital accumulation is to create new fixed and working capitals, broaden and modernize the existing ones, grow the material basis of social-cultural activities, as well as constituting the necessary resource for reserve and insurance. The process of capital accumulation forms the basis of capitalism, and is one of the defining characteristics of a capitalist economic system.

A savings and loan association (S&L), or thrift institution, is a financial institution that specializes in accepting savings deposits and making mortgage and other loans. The terms "S&L" and "thrift" are mainly used in the United States; similar institutions in the United Kingdom, Ireland and some Commonwealth countries include building societies and trustee savings banks. They are often mutually held, meaning that the depositors and borrowers are members with voting rights, and have the ability to direct the financial and managerial goals of the organization like the members of a credit union or the policyholders of a mutual insurance company. While it is possible for an S&L to be a joint-stock company, and even publicly traded, in such instances it is no longer truly a mutual association, and depositors and borrowers no longer have membership rights and managerial control. By law, thrifts can have no more than 20 percent of their lending in commercial loans—their focus on mortgage and consumer loans makes them particularly vulnerable to housing downturns such as the deep one the U.S. experienced in 2007.

The savings and loan crisis of the 1980s and 1990s was the failure of 32% of savings and loan associations (S&Ls) in the United States from 1986 to 1995. An S&L or "thrift" is a financial institution that accepts savings deposits and makes mortgage, car and other personal loans to individual members.

The wealth elasticity of demand, in microeconomics and macroeconomics, is the proportional change in the consumption of a good relative to a change in consumers' wealth. Measuring and accounting for the variability in this elasticity is a continuing problem in behavioral finance and consumer theory.

The paradox of thrift is a paradox of economics. The paradox states that an increase in autonomous saving leads to a decrease in aggregate demand and thus a decrease in gross output which will in turn lower total saving. The paradox is, narrowly speaking, that total saving may fall because of individuals' attempts to increase their saving, and, broadly speaking, that increase in saving may be harmful to an economy. The paradox of thrift is an example of the fallacy of composition, the idea that what is true of the parts must always be true of the whole. The narrow claim transparently contradicts the fallacy, and the broad one does so by implication, because while individual thrift is generally averred to be good for the individual, the paradox of thrift holds that collective thrift may be bad for the economy.

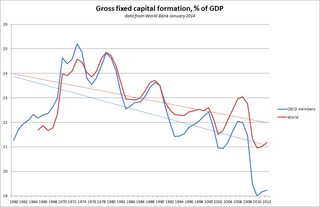

Capital formation is a concept used in macroeconomics, national accounts and financial economics. Occasionally it is also used in corporate accounts. It can be defined in three ways:

Dissaving is negative saving. If spending is greater than disposable income, dissaving is taking place. This spending is financed by already accumulated savings, such as money in a savings account, or it can be borrowed. Household dissaving therefore corresponds to an absolute decrease in their financial investments.

Under-capitalization refers to any situation where a business cannot acquire the funds they need. An under-capitalized business may be one that cannot afford current operational expenses due to a lack of capital, which can trigger bankruptcy, may be one that is over-exposed to risk, or may be one that is financially sound but does not have the funds required to expand to meet market demand.

Requires updating to reflect the current Income Tax Act and the growth of MICs that trade on the TSX.

The following outline is provided as an overview of and topical guide to finance:

In finance, an asset–liability mismatch occurs when the financial terms of an institution's assets and liabilities do not correspond. Several types of mismatches are possible. An asset-liability mismatch presents a material risk at institutions with significant debt exposure, such as banks or sovereign governments. A significant mismatch may lead to insolvency or illiquidity, which can cause financial failure. Such risks were among the principal causes of economic crises such as the 1980s Latin American Debt Crisis, the 2007 Subprime Mortgage Crisis, the U.S. Savings and Loan Crisis, and the collapse of Silicon Valley Bank in 2023.

Bank regulation in the United States is highly fragmented compared with other G10 countries, where most countries have only one bank regulator. In the U.S., banking is regulated at both the federal and state level. Depending on the type of charter a banking organization has and on its organizational structure, it may be subject to numerous federal and state banking regulations. Apart from the bank regulatory agencies the U.S. maintains separate securities, commodities, and insurance regulatory agencies at the federal and state level, unlike Japan and the United Kingdom. Bank examiners are generally employed to supervise banks and to ensure compliance with regulations.

A bank is a financial institution that accepts deposits from the public and creates a demand deposit while simultaneously making loans. Lending activities can be directly performed by the bank or indirectly through capital markets.

This article provides background information regarding the subprime mortgage crisis. It discusses subprime lending, foreclosures, risk types, and mechanisms through which various entities involved were affected by the crisis.

A global saving glut is a situation in which desired saving exceeds desired investment. By 2005 Ben Bernanke, chairman of the Federal Reserve, the central bank of the United States, expressed concern about the "significant increase in the global supply of saving" and its implications for monetary policies, particularly in the United States. Although Bernanke's analyses focused on events in 2003 to 2007 that led to the 2007–2009 financial crisis, regarding GSG countries and the United States, excessive saving by the non-financial corporate sector (NFCS) is an ongoing phenomenon, affecting many countries. Bernanke's global saving glut (GSG) hypothesis argued that increased capital inflows to the United States from GSG countries were an important reason that U.S. longer-term interest rates from 2003 to 2007 were lower than expected.

Precautionary saving is saving that occurs in response to uncertainty regarding future income. The precautionary motive to delay consumption and save in the current period rises due to the lack of completeness of insurance markets. Accordingly, individuals will not be able to insure against some bad state of the economy in the future. They anticipate that if this bad state is realized, they will earn lower income. To avoid adverse effects of future income fluctuations and retain a smooth path of consumption, they set aside a precautionary reserve, called precautionary savings, by consuming less in the current period, and resort to it in case the bad state is realized in the future.

The 2007–2008 financial crisis, or Global Economic Crisis (GEC), was the most severe worldwide economic crisis since the Great Depression. Predatory lending in the form of subprime mortgages targeting low-income homebuyers, excessive risk-taking by global financial institutions, a continuous buildup of toxic assets within banks, and the bursting of the United States housing bubble culminated in a "perfect storm", which led to the Great Recession.