Finance is the study and discipline of money, currency and capital assets. It is related to but distinct from economics, which is the study of the production, distribution, and consumption of goods and services. Based on the scope of financial activities in financial systems, the discipline can be divided into personal, corporate, and public finance.

Corporate governance are mechanisms, processes and relations by which corporations are controlled and operated ("governed").

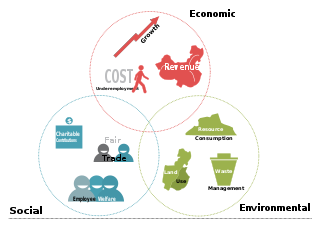

The triple bottom line is an accounting framework with three parts: social, environmental and economic. Some organizations have adopted the TBL framework to evaluate their performance in a broader perspective to create greater business value. Business writer John Elkington claims to have coined the phrase in 1994.

Cost–benefit analysis (CBA), sometimes also called benefit–cost analysis, is a systematic approach to estimating the strengths and weaknesses of alternatives. It is used to determine options which provide the best approach to achieving benefits while preserving savings in, for example, transactions, activities, and functional business requirements. A CBA may be used to compare completed or potential courses of action, and to estimate or evaluate the value against the cost of a decision, project, or policy. It is commonly used to evaluate business or policy decisions, commercial transactions, and project investments. For example, the U.S. Securities and Exchange Commission must conduct cost-benefit analyses before instituting regulations or deregulations.

Corporate social responsibility (CSR) or corporate social impact is a form of international private business self-regulation which aims to contribute to societal goals of a philanthropic, activist, or charitable nature by engaging in, with, or supporting professional service volunteering through pro bono programs, community development, administering monetary grants to non-profit organizations for the public benefit, or to conduct ethically oriented business and investment practices. While once it was possible to describe CSR as an internal organizational policy or a corporate ethic strategy similar to what is now known today as Environmental, Social, Governance (ESG); that time has passed as various companies have pledged to go beyond that or have been mandated or incentivized by governments to have a better impact on the surrounding community. In addition, national and international standards, laws, and business models have been developed to facilitate and incentivize this phenomenon. Various organizations have used their authority to push it beyond individual or industry-wide initiatives. In contrast, it has been considered a form of corporate self-regulation for some time, over the last decade or so it has moved considerably from voluntary decisions at the level of individual organizations to mandatory schemes at regional, national, and international levels. Moreover, scholars and firms are using the term "creating shared value", an extension of corporate social responsibility, to explain ways of doing business in a socially responsible way while making profits.

Monetization is, broadly speaking, the process of converting something into money. The term has a broad range of uses. In banking, the term refers to the process of converting or establishing something into legal tender. While it usually refers to the coining of currency or the printing of banknotes by central banks, it may also take the form of a promissory currency. The term "monetization" may also be used informally to refer to exchanging possessions for cash or cash equivalents, including selling a security interest, charging fees for something that used to be free, or attempting to make money on goods or services that were previously unprofitable or had been considered to have the potential to earn profits. And data monetization refers to a spectrum of ways information assets can be converted into economic value.

Social impact assessment (SIA) is a methodology to review the social effects of infrastructure projects and other development interventions. Although SIA is usually applied to planned interventions, the same techniques can be used to evaluate the social impact of unplanned events, for example, disasters, demographic change, and epidemics. SIA is important in applied anthropology, as its main goal is to be able to deliver positive social outcomes and eliminate any possible negative or long term effects.

Economic analysis of climate change is about using economic tools and models to calculate the magnitude and distribution of damages caused by climate change. It can also give guidance for the best policies for mitigation and adaptation to climate change from an economic perspective. There are many economic models and frameworks. For example, in a cost–benefit analysis, the trade offs between climate change impacts, adaptation, and mitigation are made explicit. For this kind of analysis, integrated assessment models (IAMs) are useful. Those models link main features of society and economy with the biosphere and atmosphere into one modelling framework. The total economic impacts from climate change are difficult to estimate. In general, they increase the more the global surface temperature increases. Economic analysis also looks at the economics of climate change mitigation.

In the field of accounting, when reporting the financial statements of a company, accounting constraints are boundaries, limitations, or guidelines.

Environmental accounting is a subset of accounting proper, its target being to incorporate both economic and environmental information. It can be conducted at the corporate level or at the level of a national economy through the System of Integrated Environmental and Economic Accounting, a satellite system to the National Accounts of Countries.

Return on investment (ROI) or return on costs (ROC) is the ratio between net income and investment. A high ROI means the investment's gains compare favourably to its cost. As a performance measure, ROI is used to evaluate the efficiency of an investment or to compare the efficiencies of several different investments. In economic terms, it is one way of relating profits to capital invested.

In finance, a stock index, or stock market index, is an index that measures the performance of a stock market, or of a subset of a stock market. It helps investors compare current stock price levels with past prices to calculate market performance.

Environmental, social, and governance (ESG), is a set of aspects, including environmental issues, social issues and corporate governance that can be considered in investing. Investing with ESG considerations is sometimes referred to as responsible investing or, in more proactive cases, impact investing.

Earth Economics is a 501(c)(3) non-profit formally established in 2004 and headquartered in Tacoma, Washington, United States. The organization uses natural capital valuation to help decision makers and local stakeholders to understand the value of natural capital assets. By identifying, monetizing, and valuing natural capital and ecosystem services.

Corporate finance is the area of finance that deals with the sources of funding, and the capital structure of corporations, the actions that managers take to increase the value of the firm to the shareholders, and the tools and analysis used to allocate financial resources. The primary goal of corporate finance is to maximize or increase shareholder value.

Social accounting is the process of communicating the social and environmental effects of organizations' economic actions to particular interest groups within society and to society at large. Social Accounting is different from public interest accounting as well as from critical accounting.

Triple bottom line cost-benefit analysis (TBL-CBA) is an evidence-based economic method that combines cost–benefit analysis (CBA) and life-cycle cost analysis (LCCA) across the triple bottom line (TBL) to weigh costs and benefits to project stakeholders. The TBL-CBA process quantifies total net present value, return on investment, and project payback. TBL-CBA uses location-specific data to give asset owners and design professionals the flexibility and capability to provide a rigorous analysis of investment alternatives through all stages of planning and design.

Sustainable return on investment (S-ROI) is a methodology for identifying and quantifying environmental, societal, and economic impacts of investment in projects and initiatives.

Susana Mourato is a professor of environmental economics at the London School of Economics and Political Science. She holds a leader position at the Grantham Research Institute on Climate Change and the Environment.