Related Research Articles

Tax brackets are the divisions at which tax rates change in a progressive tax system. Essentially, tax brackets are the cutoff values for taxable income—income past a certain point is taxed at a higher rate.

The United States Revenue Act of 1926, 44 Stat. 9, reduced inheritance and personal income taxes, cancelled many excise imposts, eliminated the gift tax and ended public access to federal income tax returns.

The Revenue Act of 1932 raised United States tax rates across the board, with the rate on top incomes rising from 25 percent to 63 percent. The estate tax was doubled and corporate taxes were raised by almost 15 percent.

The Revenue Act of 1913, also known as the Underwood Tariff or the Underwood-Simmons Act, re-established a federal income tax in the United States and substantially lowered tariff rates. The act was sponsored by Representative Oscar Underwood, passed by the 63rd United States Congress, and signed into law by President Woodrow Wilson.

The United States Revenue Act of 1942, Pub. L. 753, Ch. 619, 56 Stat. 798, increased individual income tax rates, increased corporate tax rates, and reduced the personal exemption amount from $1,500 to $1,200. The exemption amount for each dependent was reduced from $400 to $350.

The United States Second Revenue Act of 1940 created a corporate excess profits tax and increased corporate tax rates.

The Revenue Act of 1941 permanently extended the temporary individual, corporate, and excise tax increases of 1940, increased the excess profits tax by 10 percentage points and increased corporate tax rates 6-7 percentage points.

The United States Revenue Act of 1916, raised the lowest income tax rate from 1% to 2% and raised the top rate to 15% on taxpayers with incomes above $2 million. Previously, the top rate had been 7% on income above $500,000. The Act also instituted the federal estate tax.

The United States War Revenue Act of 1917 greatly increased federal income tax rates while simultaneously lowering exemptions.

The Revenue Act of 1918, 40 Stat. 1057, raised income tax rates over those established the previous year. The bottom tax bracket was expanded but raised from 2% to 6%.

The United States Revenue Act of 1921 was the first Republican tax reduction following their landslide victory in the 1920 federal elections. New Secretary of the Treasury Andrew Mellon argued that significant tax reduction was necessary in order to spur economic expansion and restore prosperity.

The United States Revenue Act of 1924, also known as the Mellon tax bill cut federal tax rates for 1924 income. The bottom rate, on income under $4,000, fell from 1.5% to 1.125%.

In France, taxation is determined by the yearly budget vote by the French Parliament, which determines which kinds of taxes can be levied and which rates can be applied.

The Revenue Act of 1928, formerly codified in part at 26 U.S.C. sec. 22(a), is a statute introduced as H.R. 1 and enacted by the 70th United States Congress in 1928 regarding tax policy.

The Revenue Act of 1936, 49 Stat. 1648, established an "undistributed profits tax" on corporations in the United States.

The Revenue Act of 1934 raised United States individual income tax rates marginally on higher incomes. The top individual income tax rate remained at 63 percent.

Taxes in Switzerland are levied by the Swiss Confederation, the cantons and the municipalities.

Taxes in Germany are levied at various government levels: the federal government, the 16 states (Länder), and numerous municipalities (Städte/Gemeinden). The structured tax system has evolved significantly, since the reunification of Germany in 1990 and the integration within the European Union, which has influenced tax policies. Today, income tax and Value-Added Tax (VAT) are the primary sources of tax revenue. These taxes reflect Germany's commitment to a balanced approach between direct and indirect taxation, essential for funding extensive social welfare programs and public infrastructure. The modern German tax system accentuate on fairness and efficiency, adapting to global economic trends and domestic fiscal needs.

Taxation may involve payments to a minimum of two different levels of government: central government through SARS or to local government. Prior to 2001 the South African tax system was "source-based", where in income is taxed in the country where it originates. Since January 2001, the tax system was changed to "residence-based" wherein taxpayers residing in South Africa are taxed on their income irrespective of its source. Non residents are only subject to domestic taxes.

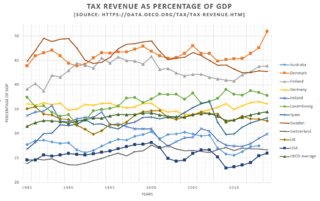

Tax revenue in Luxembourg was 38.65% of GDP in 2017, which is just above the average OECD in 2017.