Index-based insurance, also known as index-linked insurance, weather-index insurance or, simply, index insurance, is primarily used in agriculture. Because of the high cost of assessing losses, traditional insurance based on paying indemnities for actual losses incurred is usually not viable, particularly for smallholders in developing countries. With index-based insurance, payouts are related to an “index” that is closely correlated to agricultural production losses, such as one based on rainfall, yield or vegetation levels (e.g. pasture for livestock). Payouts are made when the index exceeds a certain threshold, often referred to as a “trigger”. By making payouts according to an index instead of individual claims, providers can circumvent the transaction costs associated with claims assessments. Index-based insurance is therefore not designed to protect farmers against every peril, but only where there is a widespread risk that significantly influences a farmer’s livelihood. [1] Many such indices now make use of satellite imagery. [2] [3]

Traditional insurance schemes are susceptible to morally hazardous behaviors. To ensure that a given claim is legitimate, time and resources must be allocated to adequately audit the losses or damages incurred from an event. Index-based insurance attempts to reduce costs by circumventing the issue of moral hazard, thereby eliminating the administrative costs of claims auditing. This is possible because index-based insurance insures against risks that can not significantly be manipulated through human intervention (e.g. extreme weather). [4] Unlike other insurance, adverse events cannot easily be predicted statistically, large numbers of people tend to be affected at the same time (known as "concurrency" by the insurance industry) and losses for each of them tend to be significant. The opposite is the case for more traditional insurance such as home theft insurance, where actuaries can make a good forecast of the likely incidence of claims, thefts are (relatively) rare, all the houses on a block are not entered at the same time, and entire contents of a house are not usually stolen. [5]

Insuring risk in small-scale agriculture faces particular problems that are not usually encountered by the broader insurance sector. Production relies on natural conditions, such as rain, temperature, and sunlight, which cannot be controlled easily by poorer farmers, other than by those with access to irrigation or plastic tunnels in the case of horticultural crops. Consequently farmers face problems on a regular basis. [5]

Traditional insurance has two cost categories. First is the underlying risk that is being insured and, second, the costs involved in operating the insurance, such as carrying out individual risk assessments and loss adjustments. In the agricultural sector these costs tend to be high and premiums are often unaffordable for most poorer farmers. The fixed costs of loss verification make it uneconomic to investigate losses for small-scale agriculture producers whose total insurance premiums are small. In practice, this can lead to poor loss verification, morally hazardous behavior and high loss ratios for insurance companies. [6]

In theory, index-based insurance can cover many farmers while avoiding the need for loss assessment and adjustment. This can reduce some administrative and implementation costs, and also has the potential to limit payouts caused by fraud or poor farming practices.

Although agriculture is the main application of index insurance, it can also be applied to other markets as a similar means of protection. Droughts and floods that cause water supply disruptions can lead to financial damage that, if not remedied quickly, can further snowball into long-term economic damage. Index-insurance could be used to cover the potential economic losses that might occur with water supply disruptions and similar perils that are heavily influenced by weather conditions. [7]

Another unorthodox application of index-insurance is using it as a means of hedging. The use of index insurance by financial institutions and farm input suppliers who extend credit to low income farmers in developing countries may be a more cost-effective use and enable such bulk buyers of insurance to hedge against default by farmers and thus continue to deal with those who have a high risk of defaulting. [8]

Index-based insurance does not always provide farmers with indemnities when they experience crop or animal losses and the indemnity payments sometimes do not accurately reflect the size of the losses they experience. This is because an index is based on a geographical area within which farmers may have different experiences with, e.g., rainfall. As a consequence some farmers may achieve a good crop when most others in the area experience a crop failure. However, under an index-based system all farmers receive payouts. This problem has become known as "basis risk". [9] As a direct consequence of basis risk, farmers are usually reluctant to pay the same premiums for index-based insurance that they would for standard insurance. Reducing basis risk by incorporating newly upcoming data sources is of central interest in current research. [10] [11]

There are considerable challenges that must be overcome to effectively service farmers in remote areas. The lack of historical rainfall data, yield data, or information on livestock mortality has complicated the development of indices, while the small size of farms, low value of crops or animals to be insured, and high costs of operation have made it difficult to design a workable scheme. [12] Offsetting that, ICTs, particularly smartphones, are reducing costs, while increasing use of satellite measurements for the purposes of index development has also been effective. [1] [13] [14]

Experience to date in developing countries has been that index-based insurance requires subsidies in order to be commercially viable. Subsidies usually take one of two forms: governments may support the establishment of insurance programmes through provision of data necessary to calculate indices and through assistance with promotion and training, or they may provide direct support, often by subsidizing premium payments. The question that needs to be addressed is whether such subsidies represent a good use of scarce national resources. [8]

Subsidies can reduce index insurance premiums to be moderately viable on the market, but there is still low uptake of the product amongst smallholders. One prominent barrier to entry is the high cost of insurance despite subsidies. This is because there is difficulty in assessing fair prices with data that is not verifiably accurate to the weather conditions that might arise. Additionally, an understanding of insurance by smallholders is difficult but necessary for adoption. Index insurance adds to this complexity because payouts may not occur even in poor-yielding seasons due to basis risk. Without ample financial literacy, smallholders often struggle to trust providers of index-based insurance. [4]

Not dissimilar from how farmers must set postharvest cash aside for next season's fertilizers and additional equipment, farmers must also have some level of liquidity in order to satisfy premium payments. Farmers may procrastinate in purchasing their insurance and would not have adequate liquidity to find a suitable insurance product for the season. As access to credit and liquidity might be challenging for many smallholders, adoption is made more difficult. One method of combating this procrastination is by collecting insurance premiums directly after growing seasons when farmers would have the highest capacity to pay. [4]

Insurance is a means of protection from financial loss in which, in exchange for a fee, a party agrees to compensate another party in the event of a certain loss, damage, or injury. It is a form of risk management, primarily used to protect against the risk of a contingent or uncertain loss.

A drought is a period of drier-than-normal conditions. A drought can last for days, months or years. Drought often has large impacts on the ecosystems and agriculture of affected regions, and causes harm to the local economy. Annual dry seasons in the tropics significantly increase the chances of a drought developing, with subsequent increased wildfire risks. Heat waves can significantly worsen drought conditions by increasing evapotranspiration. This dries out forests and other vegetation, and increases the amount of fuel for wildfires.

Agricultural policy describes a set of laws relating to domestic agriculture and imports of foreign agricultural products. Governments usually implement agricultural policies with the goal of achieving a specific outcome in the domestic agricultural product markets.

An agricultural subsidy is a government incentive paid to agribusinesses, agricultural organizations and farms to supplement their income, manage the supply of agricultural commodities, and influence the cost and supply of such commodities.

Weather derivatives are financial instruments that can be used by organizations or individuals as part of a risk management strategy to reduce risk associated with adverse or unexpected weather conditions. Weather derivatives are index-based instruments that usually use observed weather data at a weather station to create an index on which a payout can be based. This index could be total rainfall over a relevant period—which may be of relevance for a hydro-generation business—or the number where the minimum temperature falls below zero which might be relevant for a farmer protecting against frost damage.

Crop insurance is insurance purchased by agricultural producers and subsidized by a country's government to protect against either the loss of their crops due to natural disasters, such as hail, drought, and floods ("crop-yield insurance", or the loss of revenue due to declines in the prices of agricultural commodities.

A smallholding or smallholder is a small farm operating under a small-scale agriculture model. Definitions vary widely for what constitutes a smallholder or small-scale farm, including factors such as size, food production technique or technology, involvement of family in labor and economic impact. Smallholdings are usually farms supporting a single family with a mixture of cash crops and subsistence farming. As a country becomes more affluent, smallholdings may not be self-sufficient, but may be valued for the rural lifestyle. As the sustainable food and local food movements grow in affluent countries, some of these smallholdings are gaining increased economic viability. There are an estimated 500 million smallholder farms in developing countries of the world alone, supporting almost two billion people.

Parametric insurance is a non-traditional insurance product that offers pre-specified payouts based upon a trigger event. Trigger events depend on the nature of the parametric policy and can include environmental triggers such as wind speed and rainfall measurements, business-related triggers such as foot traffic, and more. Examples of current parametric products include the Caribbean Catastrophe Risk Insurance Facility (CCRIF), the African Risk Capacity (ARC), and the protection of coral reefs in the state of Quintana Roo in Mexico.

Climate risk is the potential for problems for societies or ecosystems from the impacts of climate change. The assessment of climate risk is based on formal analysis of the consequences, likelihoods and responses to these impacts. Societal constraints can also shape adaptation options. There are different values and preferences around risk, resulting in differences of risk perception.

The main economic products of Malawi are tobacco, tea, cotton, groundnuts, sugar and coffee. These have been among the main cash crops for the last century, but tobacco has become increasingly predominant in the last quarter-century, with a production in 2011 of 175,000 tonnes. Over the last century, tea and groundnuts have increased in relative importance while cotton has decreased. The main food crops are maize, cassava, sweet potatoes, sorghum, bananas, rice, and Irish potatoes and cattle, sheep and goats are raised. The main industries deal with agricultural processing of tobacco, tea and sugar and timber products. The industrial production growth rate is estimated at 10% (2009).

Weather risk management is a type of risk management done by organizations to address potential financial losses caused by unusual weather.

Agriculture Insurance Company of India Limited (AIC) is an Indian public sector undertaking headquartered in New Delhi. It is a government-owned agricultural insurer under ownership of the Ministry of Finance, Government of India. The company offers yield-based and weather-based crop insurance programs in almost 500 districts of India, and covers almost 20 million farmers, making it the biggest crop insurer in the world by number of farmers served.

Farm programs can be part of a concentrated effort to boost a country’s agricultural productivity in general or in specific sectors where they may have a comparative advantage. There are many different types of farm programs, with a variety of objectives and created with different economic mechanisms in mind. Some are meant to benefit farmers directly, while others seek to benefit consumers. They target food prices and quantity of food available on the market, as well as production and consumption of certain goods. Some are meant to benefit farmers directly, while others seek to benefit consumers. They target food prices and quantity of food available on the market, as well as production and consumption of certain goods.

Agriculture in India is highly susceptible to risks like droughts and floods. It is necessary to protect the farmers from natural calamities and ensure their credit eligibility for the next season. For this purpose, the Government of India introduced many agricultural social insurances throughout the country, the most important one of them being Pradhan Mantri Fasal Bima Yojana.

The Agricultural Development and Marketing Corporation, usually known as ADMARC, was formed in Malawi in 1971 as a government-owned corporation or parastatal to promote the Malawian economy by increasing the volume and quality of its agricultural exports, to develop new foreign markets for the consumption of Malawian agricultural produce and to support Malawi's farmers. it was the successor of a number of separate marketing boards of the colonial-era and early post-colonial times, whose functions were as much about controlling African smallholders or generating government revenues as in promoting agricultural development. At its foundation, ADMARC was given the power to finance the economic development of any public or private organisation, agricultural or not.

Contract farming involves agricultural production being carried out on the basis of an agreement between the buyer and farm producers. Sometimes it involves the buyer specifying the quality required and the price, with the farmer agreeing to deliver at a future date. More commonly, however, contracts outline conditions for the production of farm products and for their delivery to the buyer's premises. The farmer undertakes to supply agreed quantities of a crop or livestock product, based on the quality standards and delivery requirements of the purchaser. In return, the buyer, usually a company, agrees to buy the product, often at a price that is established in advance. The company often also agrees to support the farmer through, e.g., supplying inputs, assisting with land preparation, providing production advice and transporting produce to its premises. The term "outgrower scheme" is sometimes used synonymously with contract farming, most commonly in Eastern and Southern Africa. Contract farming can be used for many agricultural products, although in developing countries it is less common for staple crops such as rice and maize.

The Pradhan Mantri fasal bima yojana (PMFBY) launched on 18 February 2016 by Prime Minister Narendra Modi is an insurance service for farmers for their yields. It was formulated in line with One Nation–One Scheme theme by replacing earlier two schemes National Agricultural Insurance Scheme (NAIS) and Modified National Agricultural Insurance Scheme (MNAIS) by incorporating their best features and removing their inherent drawbacks (shortcomings). It aims to reduce the premium burden on farmers and ensure early settlement of crop assurance claim for the full insured sum.

Digital agriculture, sometimes known as smart farming or e-agriculture, is tools that digitally collect, store, analyze, and share electronic data and/or information in agriculture. The Food and Agriculture Organization of the United Nations has described the digitalization process of agriculture as the digital agricultural revolution. Other definitions, such as those from the United Nations Project Breakthrough, Cornell University, and Purdue University, also emphasize the role of digital technology in the optimization of food systems.

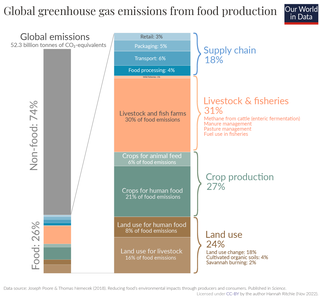

The amount of greenhouse gas emissions from agriculture is significant: The agriculture, forestry and land use sector contribute between 13% and 21% of global greenhouse gas emissions. Agriculture contributes towards climate change through direct greenhouse gas emissions and by the conversion of non-agricultural land such as forests into agricultural land. Emissions of nitrous oxide and methane make up over half of total greenhouse gas emission from agriculture. Animal husbandry is a major source of greenhouse gas emissions.

Climate risk insurance is a type of insurance designed to mitigate the financial and other risk associated with climate change, especially phenomena like extreme weather. The insurance is often treated as a type of insurance needed for improving the climate resilience of poor and developing communities. It provides post-disaster liquidity for relief and reconstruction measures while also preparing for the future measures in order to reduce climate change vulnerability. Insurance is considered an important climate change adaptation measure.