A nonprofit organization (NPO), also known as a non-business entity, not-for-profit organization, or nonprofit institution, is a legal entity organized and operated for a collective, public or social benefit, in contrast with an entity that operates as a business aiming to generate a profit for its owners. A nonprofit is subject to the non-distribution constraint: any revenues that exceed expenses must be committed to the organization's purpose, not taken by private parties. An array of organizations are nonprofit, including some political organizations, schools, business associations, churches, social clubs, and consumer cooperatives. Nonprofit entities may seek approval from governments to be tax-exempt, and some may also qualify to receive tax-deductible contributions, but an entity may incorporate as a nonprofit entity without securing tax-exempt status.

A charitable trust is an irrevocable trust established for charitable purposes and, in some jurisdictions, a more specific term than "charitable organization". A charitable trust enjoys a varying degree of tax benefits in most countries. It also generates good will. Some important terminology in charitable trusts is the term "corpus", which refers to the assets with which the trust is funded, and the term "donor", which is the person donating assets to a charity.

A foundation is a category of nonprofit organization or charitable trust that typically provides funding and support for other charitable organizations through grants, but may also engage directly in charitable activities. Foundations include public charitable foundations, such as community foundations, and private foundation, which are typically endowed by an individual or family. However, the term "foundation" may also be used by organizations that are not involved in public grantmaking.

Fundraising or fund-raising is the process of seeking and gathering voluntary financial contributions by engaging individuals, businesses, charitable foundations, or governmental agencies. Although fundraising typically refers to efforts to gather money for non-profit organizations, it is sometimes used to refer to the identification and solicitation of investors or other sources of capital for for-profit enterprises.

Tax exemption is the reduction or removal of a liability to make a compulsory payment that would otherwise be imposed by a ruling power upon persons, property, income, or transactions. Tax-exempt status may provide complete relief from taxes, reduced rates, or tax on only a portion of items. Examples include exemption of charitable organizations from property taxes and income taxes, veterans, and certain cross-border or multi-jurisdictional scenarios.

A charitable organization or charity is an organization whose primary objectives are philanthropy and social well-being.

A 501(c) organization is a nonprofit organization in the federal law of the United States according to Internal Revenue Code Section 501(c) and is one of over 29 types of nonprofit organizations exempt from some federal income taxes. Sections 503 through 505 set out the requirements for obtaining such exemptions. Many states refer to Section 501(c) for definitions of organizations exempt from state taxation as well. 501(c) organizations can receive unlimited contributions from individuals, corporations, and unions.

In the United States, a donor-advised fund is a charitable giving vehicle administered by a public charity created to manage charitable donations on behalf of organizations, families, or individuals. To participate in a donor-advised fund, a donating individual or organization opens an account in the fund and deposits cash, securities, or other financial instruments. They surrender ownership of anything they put in the fund, but retain advisory privileges over how their account is invested, and how it distributes money to charities.

Laws regulating nonprofit organizations, nonprofit corporations, non-governmental organizations, and voluntary associations vary in different jurisdictions.

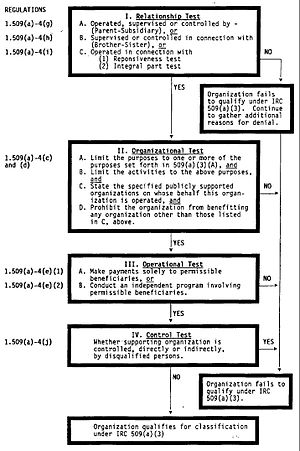

A 501(c)(3) organization is a United States corporation, trust, unincorporated association or other type of organization exempt from federal income tax under section 501(c)(3) of Title 26 of the United States Code. It is one of the 29 types of 501(c) nonprofit organizations in the US.

A donor managed investment account is a charitable giving mechanism in which donors receive a full tax deduction at the time they fund the DMI account, but retain investment management rights over the account, and can request donations from the account to charities.

The Pension Protection Act of 2006, 120 Stat. 780, was signed into law by U.S. President George W. Bush on August 17, 2006.

A private foundation is a charitable organization that, while serving a good cause, might or might not qualify as a public charity by government standards. The Bill & Melinda Gates Foundation is the largest private foundation in the U.S. with over $38 billion in assets. Most private foundations are much smaller. Out of the 84,000 private foundations that filed with the IRS in 2008, approximately 66% have less than $1 million in assets, and 93% have less than $10 million in assets. In aggregate, private foundations in the U.S. control over $628 billion in assets and made more than $44 billion in charitable contributions in 2007.

A foundation in the United States is a type of charitable organization. However, the Internal Revenue Code distinguishes between private foundations and public charities. Private foundations have more restrictions and fewer tax benefits than public charities like community foundations.

Until 1969, the term private foundation was not defined in the United States Internal Revenue Code. Since then, every U.S. charity that qualifies under Section 501(c)(3) of the Internal Revenue Service Code as tax-exempt is a "private foundation" unless it demonstrates to the IRS that it falls into another category such as public charity. Unlike nonprofit corporations classified as a public charity, private foundations in the United States are generally subject to a 1% or 2% excise tax or endowment tax on any net investment income.

Form 990 is a United States Internal Revenue Service form that provides the public with financial information about a nonprofit organization. It is often the only source of such information. It is also used by government agencies to prevent organizations from abusing their tax-exempt status. Certain nonprofits have more comprehensive reporting requirements, such as hospitals and other health care organizations.

National Philanthropic Trust(NPT) is an American independent public charity that provides philanthropic expertise to donors, foundations and financial institutions. NPT ranks among the largest grantmaking institutions in the United States.

A charitable organization in Canada is regulated under the Canadian Income Tax Act through the Charities Directorate of the Canada Revenue Agency (CRA).

Form 1023 is a United States IRS tax form, also known as the Application for Recognition of Exemption Under 501(c)(3) of the Internal Revenue Code. It is filed by nonprofits to get exemption status. On January 31st of 2020, the IRS abandoned the paper format of the form 1023. Those who used the paper version were given 90 days grace period and that ended on 30th of April 2020. Going forward, every application has to be filed online through Pay.gov portal.

A 501(h) election or Conable election is a procedure in United States tax law that allows a 501(c)(3) non-profit organization to participate in lobbying limited only by the financial expenditure on that lobbying, regardless of its overall extent. This allows organizations taking the 501(h) election to potentially perform a large amount of lobbying if it is done using volunteer labor or through inexpensive means. The 501(h) election is available to most types of 501(c)(3) organizations that are not churches or private foundations. It was introduced by Representative Barber Conable as part of the Tax Reform Act of 1976 and codified as 26 U.S.C. § 501(h), and the corresponding Internal Revenue Service (IRS) regulations were finalized in 1990.